Index-Based Insurance 2026 – Rs.72,000/Year Cover for Farmers

Index-based insurance for farmers in India is the smartest climate risk tool available to smallholder farmers in 2026 — offering automatic payouts up to Rs.72,000 per acre per season without the need for physical crop-loss inspection. With erratic monsoons, flash droughts, and unseasonal rains threatening millions of small farm holdings across 28 states, understanding how weather-index insurance works can mean the difference between financial ruin and recovery. This complete 2026 guide covers everything: what index insurance is, how RWBCIS and PMFBY differ, premium rates, eligibility criteria, the step-by-step enrolment process, who should apply, and how to claim your payout — all in one place.

- What Is Index-Based Insurance for Farmers India 2026?

- Key Facts at a Glance – RWBCIS Index Insurance

- Compensation & Premium Rate Table 2026

- Eligibility for Index-Based Crop Insurance India

- How to Enrol for Index Insurance – Step-by-Step Process

- How Index Insurance Claim Works Automatically

- Who Should Apply for Index-Based Insurance?

- PMFBY vs RWBCIS – Comparison Table 2026

- High-Value Agriculture Insurance Terms You Must Know

- Frequently Asked Questions (FAQs)

What Is Index-Based Insurance for Farmers India 2026?

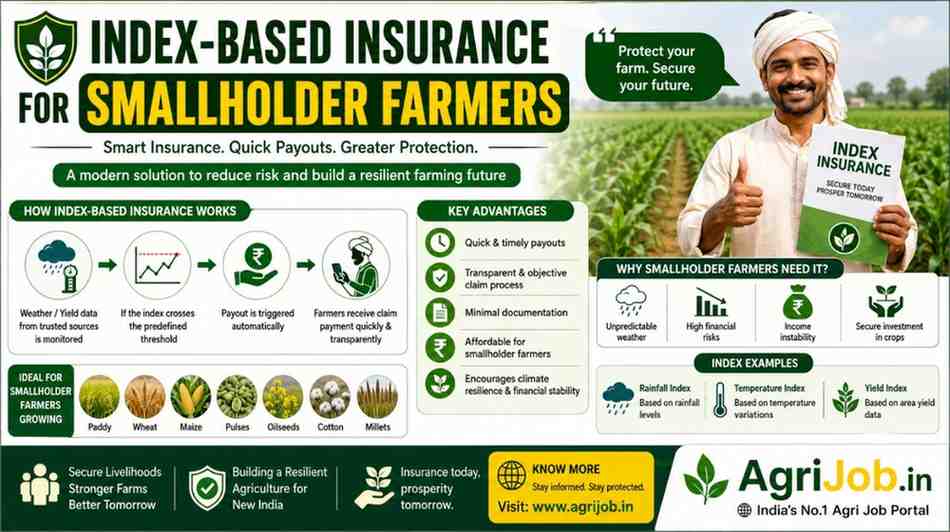

Index-based insurance for farmers India — also known as weather index insurance or parametric crop insurance — is a modern financial protection tool where payouts are triggered automatically when a pre-agreed weather index crosses a defined threshold. Unlike traditional crop insurance, which requires expensive physical field inspections, index insurance uses data from automated weather stations (AWS) and India Meteorological Department (IMD) stations to measure parameters such as cumulative rainfall, temperature extremes, wind speed, and humidity as a proxy for crop yield loss.

India’s primary index-based crop insurance programme is the Restructured Weather-Based Crop Insurance Scheme (RWBCIS), which was introduced alongside the Pradhan Mantri Fasal Bima Yojana (PMFBY) in 2016 and has been extended by the Union Cabinet until 2025-26 with a combined budget of ₹69,515.71 crore. RWBCIS uses weather triggers to compensate smallholder farmers for anticipated crop losses without the delays associated with Crop Cutting Experiments (CCEs). The scheme is administered by empanelled insurers — including the Agriculture Insurance Company of India (AIC), ICICI-Lombard, HDFC-ERGO, Bajaj Allianz, IFFCO-Tokio, and Cholamandalam MS — under the supervision of the Ministry of Agriculture and Farmers Welfare, Govt. of India.

For India’s approximately 86 million smallholder farmers — those holding less than 2 hectares — index insurance eliminates the 3 biggest barriers to crop insurance uptake: high premium cost, slow claim settlement, and complex paperwork. In 2026, the scheme covers food crops (cereals, millets, pulses), oilseeds, and annual commercial/horticultural crops across notified districts in all major agricultural states.

Key Facts at a Glance – RWBCIS Index Insurance 2026

| Scheme Name | Restructured Weather-Based Crop Insurance Scheme (RWBCIS) |

| Launched By | Ministry of Agriculture & Farmers Welfare, Govt. of India |

| Budget (2021–26) | ₹69,515.71 crore (combined with PMFBY) |

| Max Sum Insured | Rs.15,000 – Rs.72,000 per acre (crop & state dependent) |

| Farmer Premium (Kharif) | Maximum 2% of sum insured |

| Farmer Premium (Rabi) | Maximum 1.5% of sum insured |

| Premium (Commercial) | Maximum 5% of sum insured |

| Subsidy Split | Centre 50% : State 50% (NE/Himalayan States: Centre 90%) |

| Enrolment Mode | Online (pmfby.gov.in) / Bank / CSC / Insurer branch |

| Claim Settlement | Auto-triggered; direct credit to Aadhaar-linked bank account |

Index Insurance Compensation & Premium Rate Table 2026

The actual payout under index-based insurance for farmers India depends on 3 factors: the sum insured notified by the state government for a specific crop and Insurance Unit, the premium rate tier, and the severity of the weather index deviation. The table below shows indicative coverage ranges for major crop categories in 2026:

| Crop Type | Season | Farmer Premium | Indicative Sum Insured (per acre) | Annual Cover (2 seasons) |

|---|---|---|---|---|

| Paddy / Rice | Kharif | Max 2% | Rs.25,000 – Rs.40,000 | Rs.40,000 – Rs.72,000 |

| Wheat | Rabi | Max 1.5% | Rs.20,000 – Rs.35,000 | Rs.35,000 – Rs.60,000 |

| Maize | Kharif | Max 2% | Rs.18,000 – Rs.30,000 | Rs.30,000 – Rs.50,000 |

| Pulses (Tur, Moong) | Kharif / Rabi | Max 2% | Rs.15,000 – Rs.25,000 | Rs.25,000 – Rs.45,000 |

| Oilseeds (Mustard, Groundnut) | Rabi / Kharif | Max 1.5%–2% | Rs.18,000 – Rs.32,000 | Rs.30,000 – Rs.55,000 |

| Horticultural / Commercial Crops | Any | Max 5% | Rs.30,000 – Rs.72,000 | Up to Rs.72,000+ |

Note: Exact sum insured figures are notified district-wise and crop-wise by each state government before the season begins. Farmers should check their District Agriculture Officer’s (DAO) notification or visit pmfby.gov.in for the latest 2026 notified amounts.

Eligibility for Index-Based Crop Insurance India 2026

Understanding eligibility is critical before enrolling for index-based crop insurance India. The scheme has very broad coverage — designed specifically so that no Indian farmer is left out of the safety net.

Educational & Landholding Eligibility

- 🌾 All farmers including sharecroppers and tenant farmers growing notified crops in notified areas are eligible — no minimum land size required.

- 📋 Loanee farmers (those with KCC/crop loan from any scheduled bank) are enrolled compulsorily — no separate application needed.

- 🏡 Non-loanee farmers can enrol voluntarily on or before the cut-off date notified for each season.

- 📜 No education qualification is required — any literate or illiterate farmer can enrol with the help of a bank, CSC, or Jan Suvidha Kendra.

- 🗺️ Crop must be notified in the farmer’s specific Insurance Unit (village, gram panchayat, or district) for the relevant season.

- 🪪 Aadhaar number is mandatory for direct benefit transfer (DBT) of claim amount to bank account.

Age Limit & Category-Wise Premium Fee Table

| Farmer Category | Premium Rate (Kharif) | Premium Rate (Rabi) | Subsidy | Special Benefit |

|---|---|---|---|---|

| General / OBC Farmer | Max 2% of SI | Max 1.5% of SI | Centre 50% + State 50% | Standard coverage |

| SC / ST Farmer | Max 2% of SI | Max 1.5% of SI | Centre 50% + State 50% | Priority outreach; state may waive farmer share |

| Small & Marginal Farmer | Max 2% of SI | Max 1.5% of SI | Centre 50% + State 50% | Many states offer additional premium subvention |

| NE / Himalayan State Farmer | Max 2% of SI | Max 1.5% of SI | Centre 90% + State 10% | Maximum subsidy; lowest out-of-pocket cost |

| Women Farmer | Max 2% of SI | Max 1.5% of SI | Centre 50% + State 50% | Dedicated enrolment drives; SHG facilitation |

| Loanee Farmer (KCC holder) | Auto-deducted from loan | Auto-deducted from loan | Same subsidy applies | Auto-enrolled; zero manual effort needed |

How to Enrol for Index-Based Insurance – Step-by-Step 2026

Enrolling in index-based insurance for farmers India in 2026 is easier than ever, with both online and offline options available. Follow these numbered steps carefully before the seasonal cut-off date:

- Check Notified Crops & Cut-Off Date: Visit pmfby.gov.in or contact your District Agriculture Officer (DAO) to confirm which crops are notified in your Insurance Unit for the current season and the last date for enrolment.

- Gather Required Documents: Keep ready — Aadhaar card, land records (7/12 or Khasra-Khatauni), bank passbook (Aadhaar-linked), sowing certificate (for non-loanee farmers), and crop details (crop name, area sown in acres).

- Visit Bank / CSC / Insurer Branch: Non-loanee farmers can walk in to any scheduled commercial bank branch, PACS, or nearest Common Service Centre (CSC/Jan Suvidha Kendra). Loanee farmers are enrolled automatically — confirm with your bank that enrolment is active.

- Fill the Enrolment Form: Provide your name, Aadhaar number, mobile number, land survey number, crop name, and area under cultivation. Bank staff will assist with form-filling free of cost.

- Pay the Farmer’s Premium Share: Pay the applicable premium (max 2% for Kharif, 1.5% for Rabi) for your total sum insured. For a Kharif paddy farmer with Rs.30,000 sum insured on 1 acre, the premium is just Rs.600. Payment can be made by cash, UPI, or account debit.

- Collect Policy Document / Acknowledgement: Obtain a printed or SMS-based acknowledgement with your policy number, Insurance Unit, crop name, and sum insured. Save this for future reference.

- Register Mobile Number for SMS Alerts: Ensure your Aadhaar-linked mobile number is active to receive weather trigger alerts and claim credit notifications via SMS.

- Track Your Claim Online: After any adverse weather event in your Insurance Unit, log in to pmfby.gov.in or call the Krishi Rakshak Helpline 14447 to track your claim status. Payouts are credited directly to your Aadhaar-linked bank account within 2–4 weeks of a triggered weather event.

How Index Insurance Claim Works – Automatic Payout Process

One of the biggest advantages of index-based insurance for farmers India over traditional crop insurance is the automatic claim settlement process. There is no need for individual claim filing, no waiting for government inspection teams, and no lengthy paperwork. Here is how it works step by step:

- 🌡️ Weather Monitoring: Automated Weather Stations (AWS) and IMD observatories installed in or near each Insurance Unit continuously record rainfall, temperature, humidity, and wind speed throughout the season.

- 📊 Index Threshold Breach: When cumulative recorded weather data crosses a pre-defined trigger level — such as rainfall below 60% of normal for 30 consecutive days — the index threshold is considered breached and a payout event is activated.

- 🧮 Payout Calculation: The insurer calculates the payout proportionally based on the degree of deviation from the threshold. For example, a 20% rainfall deficit may trigger 40% of sum insured as compensation, while a 50% deficit triggers 80% or the full sum insured.

- 🏦 Direct Bank Transfer: The calculated claim amount is credited directly to the farmer’s Aadhaar-linked bank account via DBT within 2–4 weeks — no visits, no queues, no middlemen.

- 📱 SMS Notification: Farmers receive an SMS alert on their registered mobile number informing them of the weather trigger event, the payout amount, and the expected credit date.

- 📞 Grievance Redressal: For any discrepancy or non-receipt of payment, farmers can call Krishi Rakshak Helpline 14447 or raise a grievance on the PMFBY portal.

The WINDS (Weather Information Network Data Systems) initiative — funded through the Rs.824.77 crore FIAT (Fund for Innovation and Technology) — is expanding the network of automated weather stations across India in 2026, enabling hyper-local weather data collection at the gram panchayat level for more accurate index-insurance claim settlement. Learn more from the Department of Agriculture & Farmers Welfare (DAC&FW) and the Agriculture Insurance Company of India (AIC).

Who Should Apply for Index-Based Insurance for Farmers?

Index-based insurance for farmers India in 2026 is designed for a wide range of agricultural profiles. Here are 8 specific farmer profiles who must not miss enrolling this season:

- 🌾 Smallholder and marginal farmers (below 2 hectares) who cannot afford crop loss — even 1 failed season can push them into debt, making Rs.15,000–Rs.40,000 cover life-changing.

- 💧 Rainfed farmers in drought-prone districts of Maharashtra, Rajasthan, Madhya Pradesh, Telangana, and Karnataka — where erratic monsoons cause annual crop failure risks of 30%–60%.

- 👩🌾 Women farmers and women SHG members who often lack formal credit access — index insurance provides safety without requiring an existing KCC loan.

- 🏔️ Farmers in North-Eastern and Himalayan states (Assam, Meghalaya, Sikkim, Uttarakhand, Himachal Pradesh) where the Central Government bears 90% of the premium subsidy.

- 🌿 SC/ST tribal farmers growing rain-dependent crops in Jharkhand, Odisha, Chhattisgarh, and Andhra Pradesh who are most vulnerable to climate shocks.

- 🌰 Commercial and horticultural crop growers — mango, banana, onion, cotton, sugarcane farmers — whose per-acre income is high but weather risk is extreme.

- 🏦 KCC (Kisan Credit Card) holders who are compulsorily enrolled — but must verify their crop and area details are correctly registered by their bank before the cut-off date.

- 📱 Young agri-entrepreneurs and FPO (Farmer Producer Organisation) members who are scaling up farming operations and need bankable risk cover to attract agri-finance from NBFCs and cooperative banks.

PMFBY vs RWBCIS – Index Insurance Comparison Table 2026

Many farmers are confused about whether PMFBY or RWBCIS (index-based insurance) is better for their situation. This side-by-side comparison will help you choose the right scheme in 2026:

| Parameter | PMFBY (Yield-Based) | RWBCIS (Index-Based Insurance) |

|---|---|---|

| Basis of Payout | Actual crop yield loss (via CCE field surveys) | Predefined weather index threshold (rainfall, temp, wind) |

| Claim Settlement Speed | 2–6 months (depends on CCE completion) | 2–4 weeks (automatic trigger after season) |

| Individual Claim Required | Yes, for localised losses | No — fully automatic area-level trigger |

| Farmer Premium (Kharif) | Max 2% of sum insured | Max 2% of sum insured |

| Basis Risk | Low (actual loss measured) | Moderate (weather proxy may not match individual loss) |

| Technology Used | Satellite imagery, drones, CCE-GPS | Automated Weather Stations (AWS), WINDS network |

| Post-Harvest Cover | Yes (cyclone, unseasonal rain, up to 2 weeks) | Limited (specific perils only) |

| Best Suited For | Farmers where crop-loss is difficult to predict by weather alone | Rainfed farmers in areas with reliable AWS network |

| Transparency | Moderate (CCE results can be disputed) | High (weather data is objective and publicly verifiable) |

High-Value Agriculture Insurance Terms You Must Know – 2026

Mastering these key terms will help you navigate index-based insurance for farmers India more confidently and make better financial decisions for your farm:

- 🌧️ Basis Risk: The risk that the index payout does not perfectly match the actual farm-level loss. Basis risk is the main limitation of index insurance — a farmer may suffer a 40% yield loss but receive only 20% of sum insured if the area-wide weather index shows a smaller deviation. Choosing crops with high correlation to weather variables reduces basis risk.

- 📡 Automated Weather Station (AWS): Solar-powered electronic devices installed at specific locations to record real-time weather data (rainfall in mm, temperature in °C, wind speed in km/h). RWBCIS uses AWS data as the objective trigger for payouts — India’s WINDS programme is expanding AWS density to one per 5 km radius by 2026.

- 💰 Sum Insured (SI): The maximum amount a farmer can receive per acre per season under RWBCIS. For paddy in Maharashtra, SI may be Rs.35,000/acre; in UP, it may be Rs.42,000/acre. The SI is notified by the state government crop-wise and district-wise.

- 🌾 Kharif Crop Insurance: Coverage for monsoon-season crops (paddy, maize, soybean, cotton, groundnut) sown between June and September. Cut-off date for enrolment is typically 31 July. Annual CPC for related digital ads: Rs.40–80.

- ❄️ Rabi Crop Insurance: Coverage for winter-season crops (wheat, mustard, chickpea, lentils) sown between October and December. Cut-off date for enrolment is typically 31 December. Premium rate is capped at 1.5% of sum insured.

- 🏦 Kisan Credit Card (KCC): A revolving crop loan facility offered by commercial banks and cooperative banks to farmers. KCC holders are automatically enrolled in RWBCIS/PMFBY before the cut-off date — premium is auto-deducted from the loan account.

- 🖥️ YES-TECH (Yield Estimation System using Technology): An initiative under FIAT that uses satellite remote sensing for crop yield estimation — a complement to AWS-based index insurance, improving accuracy of area-yield calculations for PMFBY claims.

- 📊 Crop Cutting Experiment (CCE): A field-level survey method used exclusively in PMFBY (not RWBCIS) where government teams physically harvest and measure yield from sample plots to calculate average area yield. CCEs are being digitised and geo-tagged in 2026 to reduce fraud and delays.

- 🏛️ AIC of India (Agriculture Insurance Company of India): The primary public sector insurer for PMFBY and RWBCIS, established by the Govt. of India under the Ministry of Finance. AIC covers the largest number of farmers — over 3 crore — among all empanelled insurers. Visit aicofindia.com for scheme details.

- 📋 Insurance Unit (IU): The smallest geographic area for which a separate weather index is defined and a claim can be triggered under RWBCIS. An IU is typically a gram panchayat, revenue circle, block, or district — varying by state and crop.

Frequently Asked Questions – Index-Based Insurance for Farmers India 2026

What is index-based insurance for farmers in India?

Index-based insurance for farmers India is a crop protection scheme where payouts are automatically triggered when a pre-agreed weather parameter — like cumulative seasonal rainfall or maximum temperature — crosses a defined threshold, serving as a proxy for crop yield loss. India’s main index insurance programme is RWBCIS (Restructured Weather-Based Crop Insurance Scheme), which runs alongside PMFBY and is managed by the Ministry of Agriculture and Farmers Welfare, Govt. of India.

How much compensation can a farmer get under index-based insurance?

Under RWBCIS index-based insurance in 2026, the sum insured ranges from Rs.15,000 to Rs.72,000 per acre per season depending on the crop, state, and Insurance Unit notified by the state government. Farmers pay only 1.5%–2% of this sum as premium — for a Rs.30,000 sum insured paddy farmer, the Kharif premium is just Rs.600 per acre. The Government of India and state governments collectively subsidise the remaining 96%–98.5% of the actuarial premium.

Who is eligible for index-based crop insurance India?

All farmers — landowner farmers, sharecroppers, and tenant farmers — growing notified crops in notified Insurance Units are eligible for index-based crop insurance India. Loanee farmers with KCC/crop loans are enrolled compulsorily; non-loanee farmers can enrol voluntarily at any bank branch, CSC, or online at pmfby.gov.in before the seasonal cut-off date. No minimum land size or educational qualification is needed — only Aadhaar and active bank account linkage is required.

What is the premium rate for RWBCIS index insurance in 2026?

RWBCIS premium rates in 2026 are capped at a maximum of 2% of sum insured for Kharif crops, 1.5% for Rabi crops, and 5% for commercial or horticultural crops. The remainder of the actuarial (market-rate) premium is shared equally by the Central Government (50%) and State Government (50%). For farmers in NE and Himalayan states, the Central Government bears 90% — making index-based insurance near-free for tribal and mountain farming communities.

What is the difference between PMFBY and RWBCIS?

PMFBY is a yield-based scheme that compensates farmers after physical field crop cutting experiments (CCEs) assess actual area yield loss. RWBCIS is an index-based insurance scheme that pays automatically when weather parameters (rainfall, temperature, humidity) cross predefined thresholds — without any field visit. RWBCIS is faster (2–4 weeks vs 2–6 months for PMFBY), more transparent, and eliminates individual claim filing, but carries moderate basis risk where weather data may not perfectly reflect individual farm-level loss.

How does index-insurance claim settlement work automatically?

Index-based insurance for farmers India uses automated weather station (AWS) data to continuously monitor weather parameters during the crop season. When the recorded index (e.g., seasonal rainfall) crosses a predefined trigger threshold, the insurer automatically calculates the payout proportional to the deviation and credits it directly to the Aadhaar-linked bank account of all enrolled farmers in that Insurance Unit within 2–4 weeks — no individual claim application needed.

Can SC/ST and women farmers get extra benefits under index insurance?

Yes. For North-Eastern and Himalayan state farmers — where a large proportion of the population belongs to Scheduled Tribes — the Central Government bears 90% of the premium subsidy under RWBCIS index insurance, dramatically lowering the financial burden. Several state governments additionally waive the farmer’s 1.5%–2% premium share for SC, ST, small, and marginal farmers through state budget allocations. Women farmers also benefit from dedicated SHG-based enrolment camps organised by district agriculture departments.

How do I enrol for index-based insurance for farmers India online in 2026?

Enrolment for index-based insurance India in 2026 can be done online at the official PMFBY portal (pmfby.gov.in), through any scheduled commercial bank or cooperative bank branch, through Common Service Centres (CSC/Jan Suvidha Kendra), or directly through empanelled insurers like AIC of India. Carry your Aadhaar card, land records, bank passbook, and sowing details. The cut-off date for Kharif enrolment is typically 31 July; for Rabi it is 31 December each year.

For more information on India’s agricultural insurance framework, visit the Department of Agriculture and Farmers Welfare and the Agriculture Insurance Company of India (AIC).

This guide is regularly reviewed and updated for accuracy. Bookmark this page for the latest 2026 notifications on index-based insurance for farmers India.

Last Updated: May 2026