Index Insurance for Farmers 2026 – Rs.80,000 Claim Guide

Index based insurance for farmers in India is the most powerful financial safety net available to smallholder cultivators facing climate uncertainty in 2026. If you grow Kharif or Rabi crops anywhere in India’s 28 states and 8 Union Territories, a single bad season — caused by drought, flood, or unseasonal rain — can wipe out months of hard work and push your family into debt. Government-backed index insurance schemes like PMFBY and WBCIS can pay you up to Rs.80,000 per hectare in compensation, directly into your bank account via DBT, without any field inspection on your farm. India experienced extreme weather on 322 days in 2024, damaging over 4 million hectares of crops — yet less than 20% of smallholder farmers currently carry any insurance. This 2026 updated guide covers everything: what index based insurance is, how PMFBY and WBCIS work, premium rates, eligibility, compensation tables, who should enrol, step-by-step application, and all FAQs answered.

| Scheme Names | PMFBY (Area Yield Index) + WBCIS (Weather Index) |

| Nodal Ministry | Ministry of Agriculture & Farmers Welfare, Govt. of India |

| Farmers Covered | Over 5 crore farmers enrolled (2024–25 season) |

| Max Compensation | Up to Rs.80,000+ per hectare (crop & state specific) |

| Farmer Premium (Kharif) | Only 2% of Sum Insured |

| Farmer Premium (Rabi) | Only 1.5% of Sum Insured |

| Application Mode | Online (pmfby.gov.in), Bank branch, CSC Centre |

| Total Claims Paid (Since 2016) | Over Rs.1.83 lakh crore (5x farmer premium paid) |

- What Is Index Based Insurance for Farmers in India?

- PMFBY vs WBCIS – India’s 2 Index Insurance Schemes Explained

- Compensation & Premium Rates for Index Insurance 2026

- Eligibility Criteria for Index Based Crop Insurance India

- Who Should Apply for Index Based Insurance?

- How to Apply for Index Based Insurance Online – Step by Step

- Index Insurance Claim Process – How to Get Your Money

- Index Insurance vs Traditional Crop Insurance – Full Comparison

- High-Value Agricultural Insurance Terms You Must Know

- Frequently Asked Questions (FAQs)

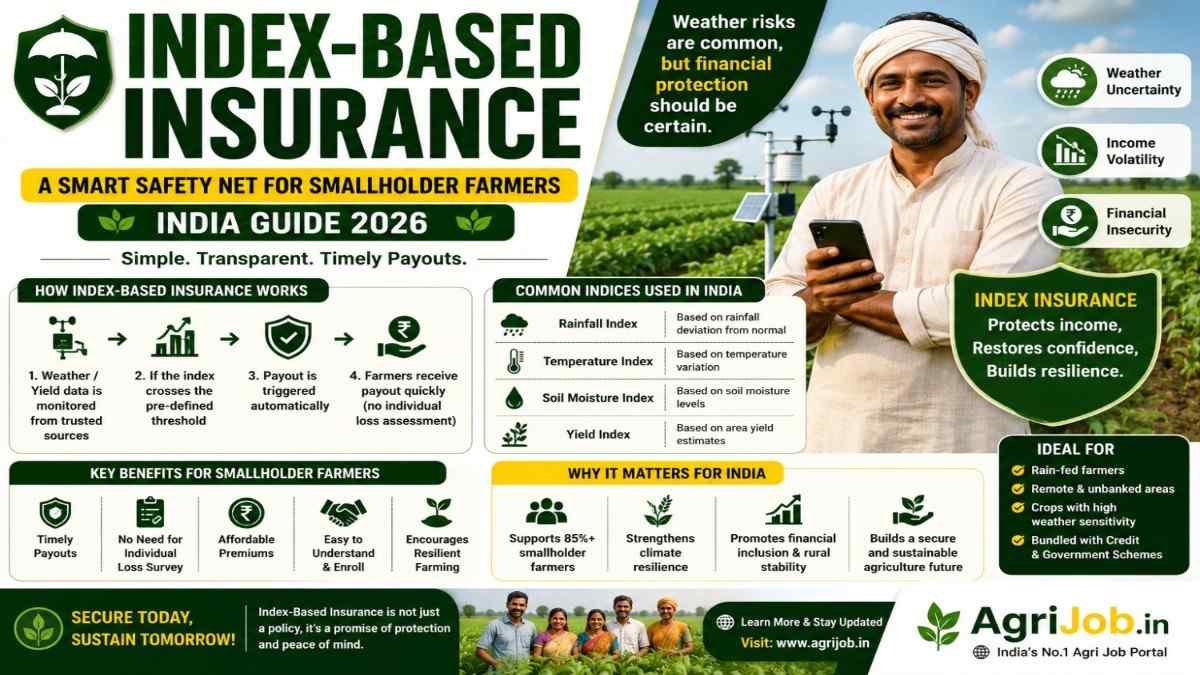

What Is Index Based Insurance for Farmers in India?

Index based insurance for farmers is a modern agricultural risk management product where compensation is paid automatically when a pre-defined measurable index — such as area-average crop yield, cumulative rainfall, or temperature — breaches a trigger threshold, regardless of what actually happened on an individual farm. There is no need for field inspectors to visit your land and assess losses crop by crop.

In India, the Govt. of India operates 2 main variants of index insurance for smallholder farmers under the umbrella of the Pradhan Mantri Fasal Bima Yojana (PMFBY) and the Weather Based Crop Insurance Scheme (WBCIS). Both are administered by the Ministry of Agriculture and Farmers Welfare and implemented through empanelled insurers including the Agriculture Insurance Company of India (AIC), ICICI Lombard, Bajaj Allianz, and other private insurers.

The key advantage of index insurance over traditional crop insurance is speed and objectivity. Since payouts are linked to verifiable data (satellite-derived yield estimates, IMD weather station readings), there is minimal scope for fraud, moral hazard, or delayed settlement. In 2026, PMFBY uses AI-assisted remote sensing and blockchain technology to make claim settlements even faster, with 80% of claims processed within 30 days.

- 🌦️ Weather Index Insurance (WBCIS): Pays out when rainfall, temperature, humidity, or wind speed at a reference IMD weather station crosses a pre-set adverse threshold. No farm visit needed — data from the nearest weather station triggers your payout automatically.

- 🌾 Area Yield Index Insurance (PMFBY): Pays out when the average crop yield for your Insurance Unit (village panchayat or taluka) falls below the threshold yield. All farmers in the same IU receive the same payout rate — fair, transparent, and tamper-proof.

- 📱 Picture-Based Insurance (PBI): A newer innovation piloted by IFPRI and HDFC ERGO that uses smartphone photos taken by farmers to verify losses, combining WBCIS weather triggers with visual ground-truth — reducing basis risk significantly.

PMFBY vs WBCIS – India’s 2 Index Insurance Schemes Explained in 2026

Understanding which form of index based insurance for farmers India is applicable in your district is critical before you enrol. Both PMFBY and WBCIS are notified by your State Government and are not available everywhere simultaneously. Here is a detailed breakdown of both schemes as updated for Kharif 2026.

PMFBY – Pradhan Mantri Fasal Bima Yojana (Area Yield Index)

Launched in 2016, PMFBY is now the world’s largest crop insurance scheme by farmer enrollment, protecting over 5 crore farmers and covering approximately 62 million hectares — nearly one-third of India’s gross cropped area. Under PMFBY, the Insurance Unit (IU) is typically a village panchayat or block, and the index used is the average crop yield measured through government-conducted Crop Cutting Experiments (CCEs). If the actual area yield falls below the threshold yield (typically the 7-year moving average), all insured farmers in that IU receive a proportional payout.

WBCIS – Weather Based Crop Insurance Scheme (Weather Index)

WBCIS was first launched in 20 states in 2007 and has since expanded across India. It uses weather parameters — rainfall, temperature, frost, relative humidity, dry spell days — recorded at the nearest IMD reference weather station as a proxy for crop performance. When these parameters cross adverse trigger levels specified in the policy, payouts are automatically calculated and disbursed. WBCIS settles claims significantly faster than PMFBY because it does not wait for CCE results, making it particularly valuable for horticulture farmers and those growing weather-sensitive crops like tur, cotton, and groundnut. WBCIS also provides additional premium benefits to SC/ST women farmers in several states.

Compensation and Premium Rates – Index Based Insurance for Farmers 2026

The financial protection available under index based insurance in India is substantial. The table below shows the farmer-payable premium rates, government subsidy, and maximum compensation available under PMFBY and WBCIS across crop categories for 2026.

| Crop Category | Farmer Premium (%) | Govt. Subsidy (%) | Typical Sum Insured (per hectare) | Max Compensation (per hectare) | Annual Premium (farmer pays) |

|---|---|---|---|---|---|

| Kharif Crops (rice, maize, tur, cotton) | 2% | 95–98% | Rs.40,000–Rs.60,000 | Up to Rs.60,000 | Rs.800–Rs.1,200 |

| Rabi Crops (wheat, mustard, gram) | 1.5% | 95–98% | Rs.35,000–Rs.55,000 | Up to Rs.55,000 | Rs.525–Rs.825 |

| Commercial / Horticultural Crops | 5% | 90–95% | Rs.60,000–Rs.1,50,000 | Up to Rs.1,50,000 | Rs.3,000–Rs.7,500 |

| Hilly / NE States (PMFBY special) | 0% (100% Govt.) | 100% | Rs.30,000–Rs.50,000 | Up to Rs.50,000 | Rs.0 (free coverage) |

Note: Actual Sum Insured is determined by the Scale of Finance (SOF) set by district-level authorities and varies by state and crop. The Rs.80,000 figure cited in Maharashtra hailstorm cases reflects higher-value crops with larger SOF. Always verify your district’s notified sum insured at pmfby.gov.in before enrolment.

Eligibility Criteria for Index Based Crop Insurance in India

The eligibility rules for index based insurance for farmers India under both PMFBY and WBCIS are broad and inclusive. The Govt. of India has deliberately kept the bar low to ensure maximum smallholder coverage. Here is a complete breakdown:

Farmer Category Eligibility

- 🌾 Landowner farmers: Any farmer who owns agricultural land and is cultivating a notified crop is eligible. Land records (Khasra, 7/12 extract) serve as proof of eligibility.

- 🤝 Tenant farmers and sharecroppers: Farmers who cultivate on leased or shared land are also fully eligible. An oral lease agreement or village patwari’s certificate is accepted as proof of insurable interest.

- 🏦 Loanee farmers (mandatory enrolment): Farmers who have taken Seasonal Agricultural Operations (SAO) loans from any scheduled bank for notified crops are enrolled automatically. The premium is deducted from the loan account.

- 📝 Non-loanee farmers (voluntary enrolment): Farmers without crop loans can voluntarily enrol before the cut-off date. They must visit a bank branch, Common Service Centre (CSC), or register online at pmfby.gov.in.

Age, Qualification & Category Eligibility Table

| Eligibility Factor | PMFBY Requirement | WBCIS Requirement |

|---|---|---|

| Minimum Age | 18 years | 18 years |

| Educational Qualification | No requirement | No requirement |

| SC/ST Farmers | Eligible; extra awareness camps by state | Eligible; SC/ST women get premium benefit |

| Women Farmers | Fully eligible; CSC camps in Bihar, UP, Odisha | Additional premium benefit in select states |

| OBC / EWS Farmers | Fully eligible | Fully eligible |

| PwBD Farmers | Fully eligible | Fully eligible |

| Application Fee | No fee (only premium applies) | No fee (only premium applies) |

| Crop Requirement | Must be a notified crop in notified area | Must be a notified crop with a reference weather station |

Who Should Apply for Index Based Insurance in India?

Index based insurance for farmers is not just for large landholders. In fact, it is most valuable for smallholder and marginal farmers who have no financial buffer to absorb a single bad harvest. If any of the following profiles match you, enrolling before the next cut-off date is a must:

- 🌱 Marginal farmers (below 1 hectare): Smallholder farmers with tiny plots face the highest financial risk from climate shocks. Index insurance pays per hectare — even a 0.5 hectare farm can receive Rs.20,000–Rs.40,000 in compensation from a single payout trigger.

- 👩🌾 Women farmers and self-help group members: Women heading farm households, including those in Bihar, UP, Odisha, and Jharkhand, can enrol through local CSC centres. WBCIS provides additional premium concessions for SC/ST women farmers in many states.

- 🤝 Tenant farmers and sharecroppers: If you cultivate someone else’s land but bear the production risk, you are legally eligible for index insurance. An oral lease certificate from the village patwari is sufficient for enrolment.

- 🌧️ Farmers in rain-fed / dryland areas: Farmers dependent entirely on monsoon rainfall — prevalent across Vidarbha (Maharashtra), Bundelkhand (UP/MP), and Rayalaseema (Andhra Pradesh) — are the most vulnerable to weather shocks. WBCIS is specifically designed for these high-risk zones.

- 🏦 Farmers with active crop loans (KCC holders): If you have a Kisan Credit Card (KCC) or crop loan from a cooperative or scheduled bank, your lender is legally required to enrol you under PMFBY. Verify your enrolment status at pmfby.gov.in.

- 🌿 Horticulture and cash crop growers: Farmers growing high-value crops — mango, banana, grapes, cotton, sugarcane — can insure under the commercial crop category for up to Rs.1,50,000 per hectare coverage under PMFBY’s add-on products.

- 🏔️ Farmers in hilly, NE, and tribal states: Farmers in Himachal Pradesh, J&K, Uttarakhand, Assam, Meghalaya, and tribal districts of Central India get 100% premium subsidy — meaning zero premium from the farmer’s pocket — under the revised PMFBY guidelines for hilly regions.

- 🌾 Young and first-generation farmers aged 18–35: Freshers entering agriculture who have taken agricultural education loans or Agri-Startup funding need protection from the very first season. Early enrolment builds a claim history that also supports future credit access from NABARD-linked programmes.

How to Apply for Index Based Insurance Online – Step by Step 2026

Applying for index based insurance for farmers in India is now a fully digital process in 2026. The official PMFBY portal has been upgraded with an Aadhaar-based e-KYC system, and the Crop Insurance App is available on both Android and iOS for seamless enrolment. Follow these 8 steps carefully:

- Check Notified Crops & Cut-off Dates: Visit pmfby.gov.in and select your State → District → Block to check which crops are notified and the last enrolment date for Kharif 2026. Each state sets its own cut-off date, typically 2 weeks after the normal sowing period.

- Gather Your Documents: Keep ready — Aadhaar card, bank passbook (must have Aadhaar-linked DBT-enabled account), land records (Khasra number, 7/12 extract or Jamabandi), sowing certificate from village patwari or Gram Panchayat, and a recent passport-size photograph.

- Calculate Your Premium: Use the premium calculator on pmfby.gov.in. Enter your crop, area under cultivation (in hectares), and season. The system will display your farmer-payable premium. Example: For 1 hectare of Kharif rice with Sum Insured of Rs.50,000, your premium is just Rs.1,000 (2%).

- Register Online (Non-Loanee Path): Create an account on pmfby.gov.in using your mobile number and Aadhaar. Complete e-KYC. Fill in the crop details, acreage, and bank account number. Upload land records. Pay the premium online via UPI, net banking, or debit card.

- Enrol Via Bank Branch: Visit your nearest bank branch (SBI, cooperative bank, or any scheduled bank) with your documents. The bank will fill your PMFBY enrolment form, deduct the premium, and provide you an enrolment acknowledgment slip with a unique policy number.

- Enrol Via Common Service Centre (CSC): All 5+ lakh CSC centres across India are authorised to process PMFBY and WBCIS enrolments. This is the best option for farmers without internet access or smartphones. The CSC operator will handle the entire process for a nominal service charge.

- Receive Policy Confirmation via SMS: Within 24–48 hours, you will receive an SMS on your registered mobile number confirming your policy number, sum insured, and crop details. Save this message as proof of enrolment.

- Download Your Policy Certificate: Log into pmfby.gov.in and download your insurance certificate. This is your official proof of coverage and is required when filing a claim.

Index Insurance Claim Process – How to Get Your Compensation

Filing a claim under index based insurance for farmers India is straightforward in 2026, especially since payouts for weather index triggers (WBCIS) and area yield triggers (PMFBY) are largely automatic and do not require individual farmers to submit damage reports. However, for mid-season adversity and post-harvest losses, you must report within the prescribed timeline. Here is the complete claim process:

- 🚨 Report Loss Within 72 Hours: For localised losses (hailstorm, flood inundation on your specific plot), call the national crop insurance helpline: 14447 or report via the Crop Insurance App within 72 hours of the loss event. Alternatively, inform your bank branch or insurance company representative.

- 📊 Automatic Trigger (WBCIS): If you are enrolled under WBCIS and the weather station data confirms an adverse index trigger, your claim is calculated automatically. You do not need to file a separate claim form — the payout is credited directly to your Aadhaar-linked bank account via DBT.

- 🌾 CCE-Based Trigger (PMFBY): For PMFBY area yield index claims, state governments conduct Crop Cutting Experiments (CCEs) after harvest. If the average yield in your Insurance Unit falls below the threshold yield, all enrolled farmers in that IU receive a payout calculated as: (Threshold Yield − Actual Yield) ÷ Threshold Yield × Sum Insured.

- 📱 Track Your Claim Status: Log into pmfby.gov.in or use the Crop Insurance App → enter your policy number or Aadhaar → check claim status in real time. In 2026, 80% of PMFBY claims are settled within 30 days of CCE completion.

- 💰 DBT to Your Bank Account: Once approved, the compensation amount is transferred via Direct Benefit Transfer (DBT) to your registered bank account. Ensure your Aadhaar is seeded to your bank account and the account is active.

Index Based Insurance vs Traditional Crop Insurance – Full Comparison

Many farmers ask: is index based insurance for farmers better than traditional indemnity-based crop insurance? The answer depends on your farm size, crop type, and location. The comparison below covers all key dimensions:

| Factor | Index Based Insurance (PMFBY / WBCIS) | Traditional Indemnity Insurance |

|---|---|---|

| How Loss Is Measured | Area-average yield or weather station data (no farm visit) | Individual farm loss assessment by surveyor |

| Claim Settlement Time | 30 days (PMFBY); faster for WBCIS | 60–120 days (waiting for survey report) |

| Farmer Premium | 1.5–2% of sum insured (heavily subsidised) | 3–8% of sum insured (market rate) |

| Maximum Compensation | Up to Rs.80,000–Rs.1,50,000 per hectare | Based on assessed loss only |

| Basis Risk | Exists — farm may lose even if IU average doesn’t trigger | Zero — loss assessed on your specific farm |

| Moral Hazard | Very low — payout not linked to individual farmer behaviour | Higher — farmer might reduce inputs after insuring |

| Government Backing | Yes — Central + State Govt. premium subsidy | Generally no (private market product) |

| Best For | Smallholder, marginal, rain-fed farmers; SC/ST women | Large commercial farms with unique high-value crops |

| Transparency | High — payout formula is pre-disclosed and objective | Moderate — depends on surveyor assessment |

High-Value Agricultural Insurance and Farming Finance Terms You Must Know

Understanding these key terms will help you navigate index based insurance for farmers in India, access better schemes, and maximise your compensation in 2026:

- 💡 Basis Risk: The risk that your individual farm suffers a loss but the area-level index does not trigger a payout. Basis risk is the main limitation of index insurance. Enrolment in WBCIS (weather station-level triggers) generally has lower basis risk than broad-area PMFBY triggers.

- 💡 Scale of Finance (SOF): The district-level valuation of crop production cost per hectare, used to determine the Sum Insured under PMFBY. A higher SOF means higher potential compensation. SOF for paddy in Punjab in 2026 is approximately Rs.72,000 per hectare.

- 💡 Threshold Yield: The average crop yield (typically a 7-year moving average) that acts as the trigger for PMFBY payouts. If the current season’s area yield falls below this figure, insured farmers receive compensation.

- 💡 Insurance Unit (IU): The geographic area for which a single index is calculated under PMFBY. Under the revised 2020 guidelines, IUs have been reduced from district-level to village panchayat level for major crops, significantly reducing basis risk for smallholders.

- 💡 Direct Benefit Transfer (DBT): The mechanism by which index insurance claims are credited directly to your Aadhaar-linked bank account, bypassing intermediaries. DBT has reduced delays and leakage in PMFBY claim settlements since 2019.

- 💡 Kisan Credit Card (KCC): A revolving credit facility for farmers, typically offering crop loans at 4–7% interest. KCC holders are mandatorily enrolled under PMFBY — check with your bank if your KCC premium is being deducted correctly each season.

- 💡 Agriculture Insurance Company of India (AIC): The primary public sector insurer for crop insurance in India, established by the Govt. of India in 2002 with NABARD as a major shareholder. AIC implements PMFBY across 500+ districts. Visit aicofindia.com for district-wise coverage details.

- 💡 NABARD (National Bank for Agriculture and Rural Development): NABARD funds rural credit flow and supports index insurance outreach through its district-level offices. For farm credit and insurance support, visit nabard.org.

- 💡 Crop Cutting Experiment (CCE): Government-supervised field trials used to measure actual crop yield at the Insurance Unit level. CCE results determine PMFBY payouts. In 2026, Smart Sampling using AI and satellite remote sensing is supplementing traditional CCEs for faster results.

- 💡 Pradhan Mantri Kisan Samman Nidhi (PM-KISAN): Farmers receiving PM-KISAN income support of Rs.6,000/year should also consider using a portion to pay their voluntary PMFBY premium, effectively amplifying their financial safety net for just Rs.800–1,200 per hectare per season.

Frequently Asked Questions – Index Based Insurance for Farmers India 2026

What is index based insurance for farmers in India?

Index based insurance for farmers in India is a crop protection scheme where payouts are triggered automatically when a measurable index — area-average yield (PMFBY) or weather parameters (WBCIS) — crosses a predefined threshold. There is no need for individual farm loss assessment. It is the world’s largest such programme, with over 5 crore Indian farmers enrolled in 2024–25.

How much compensation can I get under index based insurance?

Compensation under index based insurance for farmers depends on the Sum Insured (set by district SOF), your acreage, and the extent of index shortfall. Farmers have received up to Rs.80,000 per hectare under PMFBY for total crop failure, and up to Rs.1,50,000 per hectare for high-value horticultural crops. Since 2016, India has paid over Rs.1.83 lakh crore in total crop insurance claims — 5 times the total premiums paid by farmers.

What is the premium rate for index insurance in 2026?

For Kharif crops under PMFBY, farmers pay only 2% of the sum insured as premium. The Rabi crop rate is 1.5%, and commercial/horticultural crops are 5%. The Central and State Governments together subsidise 95–98% of the actual insurance premium. For hilly region farmers (J&K, Himachal, Northeast), the premium is 100% subsidised — meaning zero cost to the farmer.

Who is eligible for index based crop insurance in India?

All farmers — including landowners, tenant farmers, sharecroppers, and oral lessees — cultivating notified crops in notified areas are eligible. There is no age or educational qualification requirement beyond being at least 18 years old. SC/ST, OBC, EWS, women, and PwBD farmers are all fully eligible, with additional benefits for SC/ST women farmers under WBCIS in several states.

What is the difference between PMFBY and WBCIS index insurance?

PMFBY is an area yield index scheme — it pays when the average crop yield in an Insurance Unit falls below the threshold yield. WBCIS is a weather index scheme — it pays when weather station parameters (rainfall, temperature, humidity) cross adverse thresholds. WBCIS settles claims faster as it uses real-time weather data; PMFBY requires completion of Crop Cutting Experiments, which can take 2–4 months after harvest.

How do I apply for index based crop insurance online in 2026?

Visit pmfby.gov.in, register with your Aadhaar and mobile number, complete e-KYC, enter your crop and land details, and pay the premium online. Alternatively, visit any bank branch or Common Service Centre (CSC) with your Aadhaar, land records, and bank passbook. Loanee farmers (KCC holders) are enrolled automatically by their bank — verify your enrolment status each season.

Does index insurance cover all types of crop losses?

Index based insurance for farmers covers losses from drought, flood, hailstorm, cyclone, pest attack, and disease throughout the crop cycle (prevented sowing to post-harvest). It does NOT cover market price risk, losses from theft, or damage due to inadequate crop management. Individual losses that do not move the area-level index (basis risk) are also not covered — this is the primary limitation of the index approach.

What documents are needed to file an index insurance claim?

For WBCIS and automatic index triggers, no separate claim documents are needed — the payout is automatically calculated and disbursed via DBT. For PMFBY mid-season adversity claims or post-harvest losses due to localised events, you need: Aadhaar card, policy/enrolment number, bank account passbook, and a loss report filed within 72 hours via the 14447 helpline or the Crop Insurance App. The Ministry of Agriculture official portal provides state-wise claim forms and contact details.

For the latest government notifications on index based insurance for farmers India, visit the official portals: pmfby.gov.in | india.gov.in | agricoop.nic.in.

This guide is regularly reviewed and updated for accuracy. Bookmark this page for the latest 2026 notifications on index insurance for farmers in India.

Last Updated: May 2026