Agricultural Microfinance India 2026 – How Rural Fintech Is Disrupting Farm Lending | Complete Guide

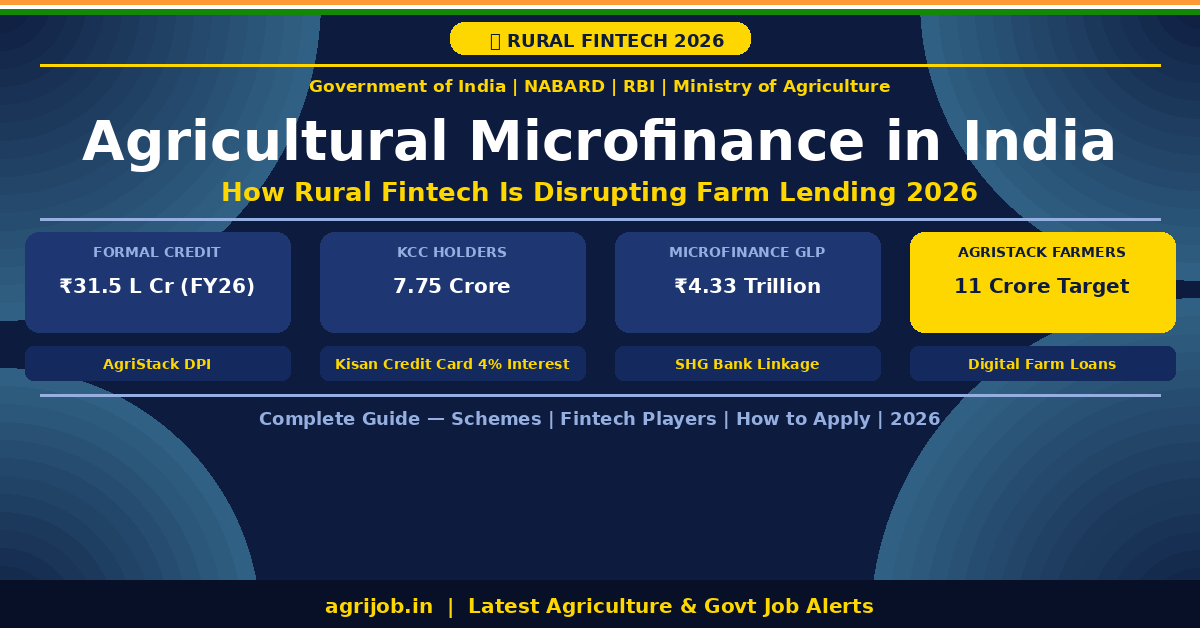

Agricultural Microfinance India 2026 is at the centre of a financial revolution that is reshaping how India’s 12.5 crore farming households access credit, insurance, and market linkages. From AI-powered loan approvals to satellite-based credit scoring, rural fintech startups — backed by the Government of India, NABARD, and RBI — are dismantling the decades-old barriers that kept small and marginal farmers trapped in informal debt. With formal institutional credit expected to exceed ₹31.5 lakh crore by FY 2025–26, this is the most transformative moment in India’s agricultural finance history. Read on for the complete guide and apply via agrijob.in.

Table of Contents

Agricultural Microfinance India 2026 – Quick Overview

| Detail | Information |

|---|---|

| Topic | Agricultural Microfinance & Rural Fintech in India 2026 |

| Governed By | Government of India | NABARD | RBI | Ministry of Agriculture |

| Key Schemes | KCC, SHG Bank Linkage, MISS, PM-KISAN, AgriStack/DAM, CSS-FPO |

| KCC Interest Rate | 4% p.a. effective (after 3% interest subvention) |

| KCC Loan Limit | Up to ₹3 Lakh (short-term crop loans) |

| Microfinance GLP (FY24) | ₹4.33 Trillion (24.5% YoY growth) |

| KCC Holders (March 2024) | 7.75 Crore active KCCs |

| AgriStack Farmer IDs | 8.62 Crore created; target 11 Crore |

| Digital Agriculture Mission Budget | ₹2,817 Crore |

| Formal Credit Target (FY26) | ₹31.5+ Lakh Crore |

| Fintech Startups (Agri-Lending) | 200+ active platforms |

| Official Portals | nabard.org | pmkisan.gov.in | nabfpo.in |

What is Agricultural Microfinance India 2026? The Big Picture

Agricultural Microfinance India 2026 refers to the ecosystem of small-ticket, collateral-light, and digitally-delivered financial products designed specifically for India’s farming and rural communities. Unlike conventional bank loans that require land records, CIBIL scores, and weeks of processing, agricultural microfinance uses group liability (Self-Help Groups and Joint Liability Groups), digital identity (Aadhaar, AgriStack Farmer ID), and AI-powered risk models to deliver credit to farmers who were previously “credit invisible.”

India’s agriculture sector contributes approximately 18.2% of GDP at constant prices and employs nearly half the national workforce. Yet, as of 2003, only 27% of rural farming households in states like Tamil Nadu had access to formal credit — a figure that has improved dramatically but still leaves millions behind. The 2026 landscape is defined by three converging forces: government digital infrastructure (AgriStack), regulated microfinance expansion (NBFC-MFIs), and technology-first fintech startups (Samunnati, Jai Kisan, DeHaat, AgroStar, Ninjacart).

Government Schemes Powering Agricultural Microfinance India 2026

The Government of India has built an interlocking set of schemes that together form the backbone of Agricultural Microfinance India 2026. Here is a complete breakdown:

1. Kisan Credit Card (KCC) – The Cornerstone of Farm Credit

The Kisan Credit Card, launched in 1998 by NABARD and RBI, is a revolving credit facility that functions like a credit card but is specifically designed for farmers’ agricultural and allied needs. As of March 2024, 7.75 crore KCCs were operational, and nearly 5.9 crore farmers have been mapped under the Mission for Saturation of KCC (MISS KCC) scheme through the Kisan Rin Portal.

| Feature | Details |

|---|---|

| Loan Limit | Up to ₹3 Lakh (short-term); Budget 2025 raised ceiling to ₹5 Lakh |

| Interest Rate | Base: 7% p.a. | Effective: 4% p.a. (after 3% subvention for prompt repayment) |

| Eligibility | Individual farmers, tenant farmers, oral lessees, sharecroppers, SHGs, JLGs |

| Coverage | Crop loans, post-harvest expenses, equipment, allied activities (dairy/fisheries) |

| Insurance | Mandatory ₹50,000 accident insurance; crop insurance linkage (PMFBY) |

| Validity | 5 years (with annual review and renewal) |

| Digital Access | ATM/PoS/mobile handsets; apply via pmkisan.gov.in |

| Processing Fee | NIL up to ₹3 Lakh limit |

2. Modified Interest Subvention Scheme (MISS) – 4% Loans for 77 Million Farmers

Through MISS, farmers access short-term crop loans of up to ₹3 lakh at a subsidized rate of 7% from scheduled commercial banks, cooperative banks, and regional rural banks. The Central Government provides a 1.5% interest subvention to lending institutions, and farmers who repay on time receive an additional 3% Prompt Repayment Incentive (PRI) — bringing their effective rate down to just 4% annually. For animal husbandry and fisheries farmers, the same benefit is extended for loans up to ₹2 lakh. Over 77 million farmers benefit from this scheme nationally.

3. SHG Bank Linkage Programme – NABARD’s Microfinance Flagship

NABARD’s Self-Help Group (SHG) Bank Linkage Programme is one of the world’s largest microfinance initiatives. Over 60 million Indian women currently hold small, collateral-free loans through this programme, impacting approximately 300 million families across the nation. The microfinance sector’s gross loan portfolio (GLP) reached ₹4.33 trillion (₹4,33,697 crore) in FY 2023–24, a 24.5% year-on-year increase. NABARD sponsors Village Level Programmes (VLPs) with banks and State Rural Livelihoods Missions (SRLMs) to facilitate SHG credit linkage and loan repayments at the village level.

4. Digital Agriculture Mission (DAM) & AgriStack – The Game-Changer

The Digital Agriculture Mission (DAM), approved in September 2024 with an initial funding of ₹2,817 crore, is building India’s digital public infrastructure for agriculture. Finance Minister Nirmala Sitharaman described AgriStack as “one of the next UPI” initiatives in the Union Budget 2026, announcing Bharat-VISTAAR — a multilingual AI platform integrating AgriStack with ICAR’s best-practice agricultural packages.

| AgriStack Component | Target | Status (2026) |

|---|---|---|

| Farmer ID (Digital Identity) | 11 Crore farmers | 8.62 Crore IDs created |

| Crop Sown Registry | 30 Crore farm plots / 604 districts | 70%+ coverage in several states |

| Geo-referenced Village Maps | All districts | Target completion: March 2027 |

| Kharif DCS (Digital Crop Survey) | 436 districts | Conducted Kharif 2024 |

| DAM Budget | ₹2,817 Crore | Approved Sep 2024 |

AgriStack’s Farmer Registry provides each farmer with a unique digital ID (similar to Aadhaar), which lenders can use to instantly verify identity, land ownership, and crop history — eliminating the fraud and document forgery that has long plagued agricultural credit. By 2026–27, DAM aims to cover 11 crore farmers as a “single source of truth” for lenders.

5. NABARD Invests in Rural Fintech – eKCC Platform

In a landmark move in April 2026, NABARD acquired a 10% equity stake in 24×7 Moneyworks Consulting Pvt. Ltd., a next-generation agri-fintech startup — NABARD’s first-ever investment in a bootstrapped startup. The startup’s flagship platform, eKisanCredit (eKCC), is a fully digital loan origination system for Cooperative Banks, PACS, and RRBs, integrating seamlessly with land records, Aadhaar, eKYC, core banking systems, and ePACS to automate the rural credit lifecycle end-to-end.

How Rural Fintech Is Disrupting Agricultural Microfinance India 2026

Conventional banks struggle with last-mile farm financing due to the absence of farm-level data and high transaction costs. Fintech platforms are solving this with three breakthrough approaches:

- Full-Stack Agri Platforms (DeHaat, AgroStar, Ninjacart): These platforms have integrated finance into the agricultural value chain. They offer input financing for fertilizers, seeds, and pesticides through their apps — with credit repaid from harvest proceeds. This eliminates the need for separate loan applications and matches credit repayment to income cycles.

- Specialized Credit Underwriters (Samunnati, Jai Kisan, Agriwise): These companies focus exclusively on agricultural finance, using AI-powered credit engines to approve small-ticket loans within 48 hours. They also offer Warehouse Receipt Financing (WRF) — where produce stored in accredited warehouses instantly generates liquidity via a warehouse receipt, allowing farmers to wait for better prices instead of distress-selling at harvest.

- Digital Identity & Scoring (Soil Magic + Satellite Magic): Platforms now use soil health data and satellite imagery to create credit scores for farmers who have no CIBIL history. Satellites track crop growth, estimate yields, and flag weather risks — converting agricultural data into collateral that banks can underwrite against.

With over 70% of farmers owning a smartphone and UPI payments enabling instant loan disbursement and repayment, the fintech revolution in farm finance is no longer a pilot — it is operational at scale across India’s rural heartland.

Agricultural Microfinance India 2026 – Interest Rates Comparison

| Credit Channel | Interest Rate | Loan Limit | Collateral |

|---|---|---|---|

| Kisan Credit Card (KCC) | 4% p.a. (after subvention) | Up to ₹3–5 Lakh | No (up to ₹1.6L collateral-free; now ₹2L) |

| MISS Crop Loan | 4%–7% p.a. | Up to ₹3 Lakh | No (collateral-free under RBI norms) |

| SHG / JLG Microfinance | 12%–21% p.a. (NBFC-MFI) | Up to ₹3 Lakh/cycle | Group guarantee (joint liability) |

| NABARD PODF (FPO Loans) | 4.5%+ p.a. (concessional) | Up to ₹15 Crore | Project-based / partial collateral |

| Rural Fintech / NBFC Apps | 12%–24% p.a. | ₹10,000–₹5 Lakh | Digital / AI-based assessment |

| Informal Moneylenders | 24%–60%+ p.a. | Variable | Land / assets / social pressure |

The RBI has recently raised the collateral-free agricultural loan limit from ₹1.6 lakh to ₹2 lakh per borrower, aligned with priority-sector lending norms. The maximum interest rate offered to microfinance borrowers in Q3 FY2026 was 21.50% — still far lower than informal moneylender rates but significantly higher than KCC’s subsidized 4%.

Eligibility for Agricultural Microfinance India 2026

- Individual Farmers: Owner-cultivators, tenant farmers, sharecroppers, oral lessees — with or without formal land records (self-declaration accepted for KCC).

- Self-Help Groups (SHGs): Groups of 10–20 members (predominantly women) operating a common savings pool and eligible for bank-linked credit.

- Joint Liability Groups (JLGs): Groups of 4–10 farmers with joint guarantee for each other’s loans — ideal for landless and tenant farmers.

- Farmer Producer Organizations (FPOs): Registered Producer Companies eligible for NABARD PODF loans up to ₹15 crore (see our previous guide at FPO Loan 2026 NABARD).

- Allied Activity Farmers: Dairy farmers, fishers, poultry farmers, beekeepers — eligible for KCC allied activity sub-limits and MISS scheme benefits up to ₹2 lakh.

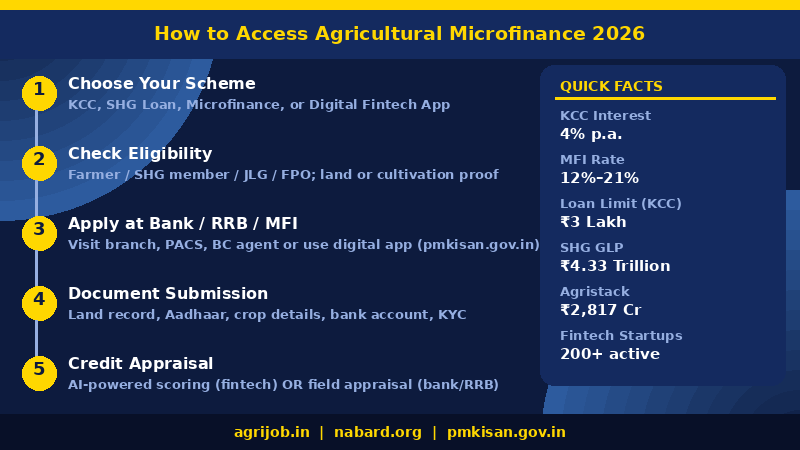

Selection Process / How to Access Agricultural Microfinance India 2026

- Identify Your Category: Determine whether you are an individual farmer, SHG member, JLG member, or FPO. This decides which scheme and which institution (bank, RRB, cooperative, NBFC-MFI, or fintech) is most appropriate.

- Choose Your Scheme: KCC (cheapest at 4%), SHG microfinance (fastest for women), JLG loan (for landless farmers), or digital fintech app loan (instant credit, higher interest).

- Apply at the Right Institution: For KCC — visit the nearest bank, RRB, cooperative bank, or apply online via pmkisan.gov.in. For SHG/JLG loans — approach your Gram Panchayat, SRLM, or district NABARD office. For digital loans — download the relevant app (Jai Kisan, AgroStar, DeHaat) and complete eKYC.

- Document Submission: Aadhaar card, land records (or self-declaration for tenant farmers), crop details, bank passbook, recent photographs.

- Credit Assessment: Bank/RRB uses field appraisal. Fintech platforms use AI, satellite data, and AgriStack Farmer ID for instant scoring.

- Loan Sanction & Disbursement: KCC approved within 14 days (Punjab/Maharashtra) to 30–60 days (UP/Odisha). Fintech apps: 48 hours. SHG loans: typically within the group’s monthly meeting cycle.

- Repayment: KCC repayment cycles align with crop harvest. SHG/JLG typically monthly installments. Fintech platforms accept UPI/AEPS repayments digitally.

How to Apply Online for Agricultural Microfinance India 2026

- Kisan Credit Card Online: Visit pmkisan.gov.in → Click “Kisan Credit Card (KCC)” under Quick Links → Fill in farmer details and Aadhaar → Bank branch contacts you for verification → Loan sanctioned.

- SHG / JLG Credit: Contact your nearest NABARD Regional Office, State Rural Livelihood Mission (SRLM) office, or block-level agriculture department. NABARD’s 2,421 Financial Literacy Centres (CFLs) across India can guide you.

- Microfinance Institution (MFI) Loan: Contact banks operating JLG/SHG microfinance like ICICI Bank (via Cashpor Micro Credit, Midland Microfin), Ujjivan SFB, Bandhan Bank, or other NBFC-MFIs in your district.

- Digital Fintech App Loan: Download apps from Jai Kisan, Samunnati, AgroStar, or DeHaat. Complete eKYC with Aadhaar and mobile OTP. AgriStack Farmer ID can pre-fill crop and land data. Loan credited directly to linked bank account within 48 hours.

- FPO Loan (Large Projects): Visit nabfpo.in and submit Concept Note to NABARD Regional Office as described in our FPO Loan guide.

Challenges in Agricultural Microfinance India 2026

Despite remarkable progress, several structural challenges remain in Agricultural Microfinance India 2026 that policymakers and fintech innovators are actively addressing:

- Credit Growth Moderation: Bank lending to agriculture and allied activities grew only 10.4% YoY as of March 2025, down from 20% a year earlier — signalling a need for deeper credit penetration.

- Tenant Farmer Exclusion: Only 45% of tenant farmers have KCCs due to documentation challenges (NITI Aayog, 2024). AgriStack’s digital self-declaration mechanism is addressing this.

- Awareness Gaps: An estimated 68% of Bihar farmers are unaware that KCC covers non-crop expenses like storage, post-harvest processing, and allied activities.

- Long-term vs Short-term Credit Imbalance: Investment credit for irrigation, storage, climate-resilient infrastructure, and mechanization continues to lag behind short-term crop loans — limiting agricultural productivity growth.

- Digital Connectivity: Despite 5G availability in most rural areas, connectivity “dark spots” still exist that prevent instant digital loan applications in remote blocks.

- MFI Interest Rates: At 12%–21%, microfinance rates are significantly higher than KCC subsidized rates, potentially burdening marginal borrowers.

Is Agricultural Microfinance India 2026 a Good Opportunity for NRIs and International Agriculture Graduates?

For NRIs returning to India with expertise in agriculture finance, fintech, or agribusiness, the current landscape represents a once-in-a-generation opportunity. India’s agricultural finance market — valued at INR 1,200 billion and growing — is actively seeking technology and capital to bridge the credit gap that still affects millions of small farmers. In an India vs USA comparison for agricultural microfinance, India’s SHG model — empowering 60 million women borrowers — is globally unmatched in scale and social impact, outperforming comparable programs in the United States (like USDA’s FSA microloan program, which is capped at $50,000 and serves far fewer beneficiaries).

For international agriculture students and diaspora investors, India’s agri-fintech sector (200+ active startups, ₹30,000 crore disbursed by alternative lending platforms) offers investment and career opportunities in credit underwriting, satellite crop monitoring, warehouse receipt financing, and rural digital payments. The Government of India’s Digital Agriculture Mission (₹2,817 crore) and AgriStack infrastructure create a fertile ecosystem for agriculture jobs in India for overseas applicants — particularly in data science, AI, and rural credit technology roles at companies like Samunnati, Jai Kisan, Farmonaut, and NABARD-backed fintechs.

Important Links – Agricultural Microfinance India 2026

| Link | URL |

|---|---|

| Apply for KCC Online | pmkisan.gov.in (KCC Quick Link) |

| NABARD SHG / Microfinance | nabard.org – Official |

| AgriStack / FPO Portal | nabfpo.in |

| Digital Agriculture Mission | agriwelfare.gov.in |

| SFAC – FPO Schemes | sfacindia.com |

| More Agriculture Schemes | Latest Agriculture Jobs & Schemes – agrijob.in |

| Latest Govt Schemes 2026 | Govt Schemes & Jobs 2026 – agrijob.in |

| Join Telegram for Updates | agrijob.in Telegram Channel |

Frequently Asked Questions about Agricultural Microfinance India 2026

Q1. What is Agricultural Microfinance India 2026?

Agricultural Microfinance India 2026 refers to the full ecosystem of small-ticket, collateral-light, and digitally-delivered financial products for India’s farming community — encompassing the Kisan Credit Card (KCC), SHG Bank Linkage Programme, JLG microfinance, NABARD PODF loans for FPOs, and rural fintech platforms that collectively aim to bridge India’s massive agricultural credit gap in 2026.

Q2. What is the cheapest farm loan available in India in 2026?

The Kisan Credit Card (KCC) with the Modified Interest Subvention Scheme (MISS) offers the most affordable crop loans — at an effective interest rate of just 4% per annum for farmers who repay on time. This is available from all scheduled commercial banks, RRBs, and cooperative banks, with no processing fee up to ₹3 lakh.

Q3. How is rural fintech disrupting agricultural microfinance in India?

Rural fintech platforms use AI-powered credit scoring, satellite imagery (for crop monitoring and yield estimation), AgriStack digital Farmer IDs, and UPI-based disbursement to approve and deliver farm loans in as little as 48 hours — compared to 30–60 days for traditional bank processing. Platforms like Jai Kisan, Samunnati, and AgroStar are leading this disruption.

Q4. What is AgriStack and how does it help farmers get loans?

AgriStack is India’s Digital Public Infrastructure (DPI) for agriculture — often called “the next UPI for farming.” It creates a unique digital Farmer ID for each of India’s 11 crore farmers, linked to land records, crop data, and Aadhaar. Banks and fintech lenders can instantly verify farmer identity, landholding, and crop history through AgriStack APIs, enabling faster, fraud-proof credit appraisal and loan disbursement.

Q5. Can women farmers and landless farmers access agricultural microfinance in India 2026?

Yes. Women farmers are the primary beneficiaries of NABARD’s SHG Bank Linkage Programme — with over 60 million women holding collateral-free microloans. Landless farmers, tenant farmers, and sharecroppers can access KCC through self-declaration of cultivation (no formal land record required) or through Joint Liability Groups (JLGs).

Q6. Can NRIs or Indian students abroad participate in India’s agricultural microfinance sector?

NRIs can invest in India’s growing agri-fintech sector through SEBI-regulated routes. International agriculture graduates returning to India can pursue careers in rural credit technology, satellite crop monitoring, and AI-based agricultural underwriting at firms like Samunnati, Jai Kisan, Farmonaut, or NABARD-backed ventures. The Digital Agriculture Mission (₹2,817 crore) is actively creating high-skilled jobs in agri-data and rural finance.

Final Thoughts on Agricultural Microfinance India 2026

The story of Agricultural Microfinance India 2026 is one of extraordinary ambition meeting practical innovation. From the 7.75 crore KCC holders accessing 4% crop credit, to the 60 million women empowered by SHG microfinance, to the 200+ fintech startups delivering 48-hour digital farm loans — India is building the most comprehensive agricultural finance ecosystem the world has ever seen. The Government’s ₹2,817 crore Digital Agriculture Mission and AgriStack’s 8.62 crore Farmer IDs are laying the digital rails for the next decade of rural credit growth. Whether you are a small farmer in Bihar, an agribusiness investor in the diaspora, or an agriculture graduate looking for career opportunities, Agricultural Microfinance India 2026 is an opportunity you cannot afford to ignore. Visit agrijob.in for more agriculture schemes, government job updates, and financial opportunities in 2026.

Disclaimer: This Agricultural jobs related information is only for the purpose of providing information to you and for Agricultural career advancement of Agricultural, Horticulture, Agronomy, Soil Science, Plant Breeding, Agriculture Marketing, Forestry, Poultry, Fisheries, Agri Business Management Graduates. We are not representing this employer or any Employment Agency nor we guarantee any employment. We do not ask candidates for any fees, Personal Information like (Bank OTP, Credit-Debit Card No, Aadhar Card OTP etc.) Please be Aware And never Share Such Information to any one or In the Name of agrijob.in. Please verify the correctness of the Agri jobs details yourself. We do not offer any guarantee on correctness of any details mentioned here. If a candidate pays any amount to anyone claiming to represent any company then it would be the responsibility of that candidate and he cannot hold us or the concerned employer responsible for such fraudulent activities.