India Agriculture Bond Market NRI Invest 2026 – Complete Guide to Rural Infrastructure Bonds

India Agriculture Bond Market NRI Invest 2026 is a question that thousands of NRIs across the USA, UK, UAE, Canada, and Australia are asking — and the answer is a clear YES. NRIs can invest in India’s agriculture and rural infrastructure bond market through multiple RBI and SEBI-regulated routes, earning 6.5% to 9% per annum in returns that far exceed what is available in their country of residence. Whether you are looking at Government Securities (G-Secs) via the Fully Accessible Route (FAR), PSU/infrastructure bonds from entities like NABARD, NHAI, REC, and PFC, or tax-saving 54EC Capital Gain Bonds, India’s bond market in 2026 offers safe, government-backed investment options with attractive yields. Read on for the complete guide at agrijob.in.

Table of Contents

India Agriculture Bond Market NRI Invest 2026 – Quick Overview

| Detail | Information |

|---|---|

| Regulatory Authority | Reserve Bank of India (RBI) + SEBI + Ministry of Finance, GoI |

| NRI Eligible? | YES — via Fully Accessible Route (FAR), NRE/NRO Demat accounts |

| Best Route for NRIs | RBI Retail Direct (rbiretaildirect.org.in) |

| G-Sec Yield (2026) | 6.5%–7.5% p.a. (10-year benchmark) |

| PSU / Infra Bond Yield | 7%–9% p.a. (NHAI, NABARD, REC, PFC bonds) |

| 54EC Capital Gain Bonds | 5%–5.75% p.a. | Tax exemption on LTCG | ₹50 Lakh limit | 5-year lock-in |

| Bharat Bond ETF | AAA-rated PSU debt | Tradeable | Diversified | ~7% yield |

| Tax on Interest (NRIs) | 5% TDS on G-Secs (FAR) | 20% TDS on corporate/PSU bonds | DTAA benefits available |

| Investment Cap | No ceiling on G-Secs via FAR | ₹50 Lakh on 54EC bonds |

| Repatriation | Full repatriation if invested through NRE account | NRO: up to USD 1 million/year |

What is India’s Agriculture Bond Market? – Full Explanation 2026

India’s agriculture and rural bond market encompasses a wide ecosystem of government-backed and PSU-issued debt instruments that fund everything from irrigation canals and rural roads to cold storage, warehouses, and agro-processing infrastructure. At the apex is the Reserve Bank of India (RBI), which regulates government securities and the Fully Accessible Route. NABARD (National Bank for Agriculture and Rural Development) is the largest institution channelling credit into rural infrastructure through its Rural Infrastructure Development Fund (RIDF) — currently at a corpus of ₹35,000 crore under RIDF Tranche XXXI (2025–26).

The RIDF, instituted in 1995–96, has provided cumulative funding of over ₹4,98,411 crore across more than 39 eligible activities including irrigation, rural connectivity, watershed development, cold storage, seed farms, rural market yards, and social infrastructure. It is funded by the shortfall in priority-sector lending by commercial banks, as directed by RBI. NABARD also runs the NABARD Infrastructure Development Assistance (NIDA) programme for projects outside RIDF scope.

While RIDF itself is a government-to-government fund (not directly open to retail investors or NRIs), the bonds and securities issued by NABARD, and the PSUs that fund rural infrastructure — such as NHAI, REC, PFC, and IRFC — are fully accessible to NRIs through SEBI-regulated secondary markets and the RBI Retail Direct platform.

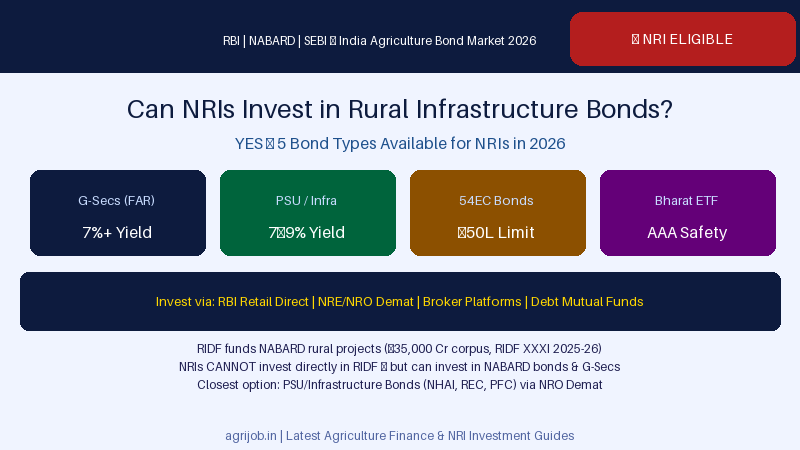

Can NRIs Invest in Rural Infrastructure Bonds in India? – 2026 Rules

The short answer is yes — NRIs can invest in India’s rural and agriculture-linked bonds through multiple legally approved routes. Here is the definitive breakdown for NRIs investing in India vs USA/UK bond markets in 2026:

| Bond Type | NRI Eligible? | Yield (2026) | Route | Tax Benefit |

|---|---|---|---|---|

| Government Securities (G-Secs) | ✅ YES (FAR) | 6.5–7.5% p.a. | RBI Retail Direct / NRO Demat | 5% TDS; DTAA reducible |

| State Development Loans (SDLs) | ✅ YES | ~7% p.a. | RBI Retail Direct | 5% TDS |

| Treasury Bills (T-Bills) | ✅ YES (91/182/364 day) | Capital gain (short term) | RBI Retail Direct | STCG Tax |

| PSU Bonds (NHAI, REC, PFC, NABARD) | ✅ YES | 7–9% p.a. | NRO Demat via broker | 20% TDS; Sec 10(15) exemption possible |

| 54EC Capital Gain Bonds | ✅ YES | 5–5.75% p.a. | NRO account / broker | LTCG tax exemption (Sec 54EC) |

| Bharat Bond ETF/FOF | ✅ YES | ~7% p.a. | NRO Demat / Mutual Fund platforms | LTCG at 10% after 3 years |

| RIDF (NABARD’s Rural Fund) | ❌ NO (State Govt only) | Bank Rate – 1.5% | Not available to retail/NRI investors | N/A |

| Floating Rate Savings Bonds (FRSB) | ❌ NO (Resident only) | ~8% p.a. | Not NRI eligible | N/A |

| Sovereign Gold Bonds (SGBs) | ❌ NO (New issue) | 2.5% + gold price | Existing holdings can be held to maturity | N/A for new purchase |

Fully Accessible Route (FAR) – NRI Investment in G-Secs 2026

The Fully Accessible Route (FAR), introduced by RBI in 2020, is the most important development for NRI bond investors in India. Under FAR, any person resident outside India — including NRIs and OCIs — can invest in specified Government Securities (G-Secs) without any investment ceiling. This was a landmark liberalisation of India’s bond market.

FAR-designated bonds include long-dated G-Secs (5-year, 10-year, 30-year), State Development Loans (SDLs), and Treasury Bills. The RBI Retail Direct platform (rbiretaildirect.org.in), launched in 2021, allows NRIs to invest directly in these instruments with zero commission and zero brokerage. India’s 10-year G-Sec yield in 2026 is approximately 6.5%–7.5% per annum — significantly higher than US 10-year Treasuries (~4.5%), UK Gilts (~4.3%), or UAE bonds.

NABARD Bonds and Rural Infrastructure Investment for NRIs 2026

NABARD (National Bank for Agriculture and Rural Development) is India’s premier institution for rural and agricultural credit. NABARD raises funds through the bond market to finance rural infrastructure. NRIs can invest in NABARD bonds issued in the secondary market through NRO Demat accounts and broker platforms. These bonds carry high credit ratings and yields typically in the 7%–8% per annum range.

NABARD’s RIDF has reached a total cumulative allocation of ₹4,98,411 crore (including ₹18,500 crore under Bharat Nirman) since its inception in 1995–96. The annual corpus under RIDF XXXI (2025–26) stands at ₹35,000 crore. While NRIs cannot directly invest in RIDF (it is a state-government-directed fund), NABARD’s market borrowings — through which it funds NIDA and other programmes — are accessible via listed bonds.

PSU & Infrastructure Bonds for NRIs – NHAI, REC, PFC, IRFC 2026

Public Sector Undertaking (PSU) bonds are issued by government-majority-owned companies to fund large infrastructure projects — many of which directly serve the agricultural and rural sector. The key issuers for NRIs to know are:

- NHAI (National Highways Authority of India): Rural road connectivity bonds — directly improve farm-to-market access. 54EC Capital Gain Bonds also issued by NHAI.

- REC (Rural Electrification Corporation): Funds rural electrification projects. Issues 54EC Capital Gain Bonds. Yields ~7.5–8.5% p.a.

- PFC (Power Finance Corporation): Funds rural power infrastructure. Competitive yields and AAA credit rating.

- IRFC (Indian Railway Finance Corporation): Funds rural railway connectivity. Listed bonds accessible to NRIs.

- NABARD: Agriculture and rural development financing. Bonds available via secondary market.

- HUDCO (Housing & Urban Development Corporation): Legacy tax-free bonds available in secondary market (pre-2016 issuances).

PSU bonds from these entities typically yield 7%–9% p.a., carry AAA or AA+ credit ratings, and have tenures ranging from 5 to 15 years. NRIs can buy these through any SEBI-registered broker via their NRO Demat account.

54EC Capital Gain Bonds – Best Tax-Saving Option for NRIs Selling Property 2026

If you are an NRI who has sold property in India and are sitting on long-term capital gains, Section 54EC Capital Gain Bonds are the most powerful tax-saving instrument available to you in 2026. Here is how they work:

- Invest up to ₹50 Lakh per financial year in 54EC bonds within 6 months of the property sale

- The entire long-term capital gain becomes 100% tax-exempt in India

- Eligible issuers: NHAI, REC, PFC (all fund rural/agriculture infrastructure)

- Interest rate: 5%–5.75% per annum, paid annually

- Lock-in period: 5 years (cannot be sold or pledged)

- Minimum investment: ₹10,000 (in multiples of ₹10,000)

- These bonds are directly linked to rural and agriculture infrastructure — your investment funds roads, power, and highways that serve India’s farmers

Bharat Bond ETF – Easiest Way for NRIs to Invest in PSU Debt 2026

The Bharat Bond ETF is a government-launched exchange-traded fund that invests exclusively in bonds of Central Public Sector Enterprises (CPSEs) and Public Sector Enterprises (PSEs). It is rated AAA, is highly liquid, and trades on NSE/BSE like a stock. NRIs can invest via their NRO Demat account through any SEBI-registered broker or mutual fund platform.

Key features for NRIs: ~7% yield, transparent portfolio (all PSU bonds), fixed maturity tranches (April 2030, April 2031, April 2032), LTCG taxed at 10% after 3 years, available via SIP through Bharat Bond FOF (Fund of Fund). This is the simplest way for NRIs to get exposure to India’s agriculture and rural PSU sector without researching individual bonds.

Step-by-Step: How NRIs Can Invest in India Agriculture Bonds 2026

- Open an NRE or NRO Bank Account: NRE for repatriable investments (tax-free interest); NRO for non-repatriable income from India. Required at any scheduled commercial bank — SBI, HDFC, ICICI, Axis, Kotak, etc.

- Open an NRI Demat Account: Link your NRE/NRO account to a SEBI-registered broker’s NRI Demat account. Zerodha (for NRIs via Interactive Brokers), ICICI Direct, HDFC Securities, Kotak Securities all support NRI Demat.

- Register on RBI Retail Direct: Visit rbiretaildirect.org.in. Provide PAN, Aadhaar/CKYC, NRO account details, mobile number. KYC approval takes 5–7 working days for NRIs. Once approved, buy G-Secs, SDLs, and T-Bills directly at zero commission.

- Submit DTAA Documents: Provide a Tax Residency Certificate (TRC) from your country of residence to your bank/broker. This enables reduced TDS rates under the Double Taxation Avoidance Agreement (DTAA). India has DTAAs with USA, UK, UAE, Canada, Australia, Singapore, and 80+ countries.

- Choose Your Bond Type: G-Secs via FAR for sovereign safety; PSU bonds (NHAI, REC, PFC) for higher yield; 54EC bonds for LTCG tax saving; Bharat Bond ETF for simplicity and diversification.

- Monitor and File ITR: Track interest payments (usually semi-annual). File Indian ITR annually to claim TDS refunds where applicable. Use Form 15CA/15CB for repatriation above ₹5 Lakh from NRO accounts.

Tax Rules for NRIs Investing in India Bonds 2026

| Bond Type | TDS Rate (NRI) | DTAA Benefit | Capital Gains Tax |

|---|---|---|---|

| G-Secs via FAR | 5% on interest | Yes (TRC required) | 10% LTCG (after 12 months) |

| PSU / Infra Bonds | 20% on interest | Yes (TRC required) | 10% LTCG (after 12 months) |

| 54EC Capital Gain Bonds | Interest taxable at slab rate | Yes | LTCG Exempt (property sale proceeds) |

| Bharat Bond ETF | As per debt MF rules | Yes | 10% LTCG (after 3 years, from AY 2026–27) |

| Tax-free Bonds (legacy, pre-2016) | No TDS on interest | N/A | 10% LTCG on sale |

Important note from AY 2026–27: The indexation benefit on debt funds and bonds has been removed. All LTCG on bonds (held over 12 months) is taxed at a flat 10% without indexation for NRIs and residents alike. File Form 15CA and Form 15CB for repatriation of proceeds above ₹5 Lakh from NRO accounts.

India Agriculture Bond vs USA/UK/UAE Bond – Why NRIs Choose India 2026

For NRIs investing from the USA, UK, Canada, or UAE, the India vs USA bond market comparison strongly favours Indian bonds in 2026. Here is a direct comparison that international investors and NRIs returning to India should consider:

| Market | 10-Year Govt Bond Yield | Agri/Rural PSU Bond Yield | Investment Safety |

|---|---|---|---|

| India (G-Sec FAR) | 6.5–7.5% p.a. | 7–9% p.a. (PSU bonds) | Sovereign / AAA |

| USA (Treasury) | ~4.5% p.a. | 3–5% (Muni bonds) | Sovereign |

| UK (Gilts) | ~4.3% p.a. | ~5% (infrastructure bonds) | Sovereign |

| UAE (Govt bonds) | ~4.8% p.a. | Limited agri bond market | Sovereign |

| Canada (Govt bonds) | ~3.9% p.a. | ~5% (farm credit bonds) | Sovereign |

For international students of agriculture in India from abroad, and for overseas Indian agriculture graduates returning home, India’s bond market represents an exceptional opportunity to park savings at sovereign-backed rates that are 2–3 percentage points higher than home-country alternatives. For the 32+ million NRIs and OCIs worldwide, the India agriculture bond market in 2026 is a compelling fixed-income destination.

NABARD RIDF XXXI 2025–26 – What Rural Infrastructure Gets Funded

Understanding what NABARD’s RIDF funds helps NRI investors appreciate what their PSU bond investments ultimately support. The 39 eligible activities under RIDF include:

- Agriculture sector: Minor/micro irrigation, watershed development, soil conservation, seed farms, horticulture, agri testing labs, rural market yards, cold storage, godowns, fishing harbours

- Rural connectivity: Rural roads, bridges, boats and jetties

- Social sector: Rural drinking water, rural sanitation, primary schools, rural health centres, anganwadis

- Others: Mini hydel power plants, system improvement in power sector, flood protection works

Under RIDF XXXI (2025–26), NABARD has an annual corpus of ₹35,000 crore. Historically, the agriculture/irrigation sector accounts for the largest share of RIDF sanctions — directly improving water availability, crop productivity, and farmers’ income across India’s 6.4 lakh villages.

Important Links – India Agriculture Bond Market NRI Investment 2026

| Resource | Link |

|---|---|

| RBI Retail Direct – Buy G-Secs & T-Bills | rbiretaildirect.org.in |

| NABARD Official Website | nabard.org |

| NABARD RIDF Details | NABARD RIDF Page |

| SEBI – NRI Investment Guidelines | sebi.gov.in |

| NHAI 54EC Capital Gain Bonds | nhai.gov.in |

| REC Capital Gain Bonds | recindia.nic.in |

| More Agriculture Finance Guides | Agriculture Jobs & Finance 2026 |

| Government Schemes 2026 | Govt Jobs & Schemes 2026 |

| Join Telegram for Daily Alerts | agrijob.in Telegram Channel |

Frequently Asked Questions about India Agriculture Bond Market NRI Invest 2026

Q1. What is India Agriculture Bond Market NRI Invest 2026?

India Agriculture Bond Market NRI Invest 2026 refers to the range of government-backed and PSU bond instruments available to Non-Resident Indians for investing in India’s agriculture, rural infrastructure, and development finance sector. Key options include G-Secs via RBI’s Fully Accessible Route (FAR), NABARD/NHAI/REC/PFC bonds, 54EC Capital Gain Bonds, and the Bharat Bond ETF.

Q2. Can NRIs invest directly in NABARD’s RIDF (Rural Infrastructure Development Fund)?

No. NABARD’s RIDF is funded by shortfalls from commercial banks’ priority-sector lending and is disbursed as loans to State Governments and state-owned corporations. It is not a retail investment product. However, NRIs can invest in NABARD bonds issued in the secondary market through NRO Demat accounts, which provide indirect exposure to rural infrastructure financing.

Q3. Which is the best bond option for NRIs interested in India’s agriculture sector in 2026?

For maximum yield and rural sector exposure: PSU bonds from NABARD, REC, or NHAI offering 7–9% p.a. For simplicity: Bharat Bond ETF (AAA PSU debt, tradeable). For tax saving after property sale: 54EC Capital Gain Bonds from NHAI/REC. For sovereign safety at zero commission: G-Secs via RBI Retail Direct.

Q4. How do NRIs invest in India government bonds via RBI Retail Direct?

Register at rbiretaildirect.org.in with PAN, NRO savings account, and CKYC/Aadhaar. KYC takes 5–7 days for NRIs. Once approved, you can buy G-Secs, T-Bills, and SDLs directly at zero commission, with no investment ceiling under the Fully Accessible Route (FAR).

Q5. What tax does an NRI pay on Indian bond interest in 2026?

G-Sec interest via FAR attracts 5% TDS. PSU/corporate bond interest attracts 20% TDS. Both can be reduced under DTAA by providing a Tax Residency Certificate (TRC). For 54EC bonds, the primary benefit is LTCG tax exemption on property sale, not interest exemption. File Indian ITR to claim any excess TDS as a refund.

Q6. Can NRIs in the USA, UK, or UAE invest in India agriculture bonds and repatriate the returns?

Yes. Bonds purchased through an NRE account allow full repatriation of principal and interest. For NRO-account-based investments, repatriation is allowed up to USD 1 million per financial year after tax compliance. India has DTAAs with the USA, UK, UAE, Singapore, Canada, Australia, and 80+ countries that reduce double taxation burdens.

Final Thoughts on India Agriculture Bond Market NRI Invest 2026

India Agriculture Bond Market NRI Invest 2026 is no longer a niche concept — it is a mainstream, fully regulated opportunity offering returns of 6.5%–9% per annum in a sovereign-backed market that is growing faster than any comparable bond market in the developed world. Whether you are an NRI in the US, UK, UAE, or Canada looking to diversify into India’s booming agricultural and rural infrastructure sector, the tools are in place: RBI Retail Direct for G-Secs, SEBI-regulated brokers for PSU bonds, and NHAI/REC for tax-saving 54EC instruments. With NABARD channelling ₹35,000 crore into rural India annually and the bond market expanding rapidly, your investment directly fuels India’s agricultural transformation. Start small, stay compliant, and visit agrijob.in for more agriculture finance guides and government scheme updates in 2026.

Disclaimer: This Agricultural jobs related information is only for the purpose of providing information to you and for Agricultural career advancement of Agricultural, Horticulture, Agronomy, Soil Science, Plant Breeding, Agriculture Marketing, Forestry, Poultry, Fisheries, Agri Business Management Graduates. We are not representing this employer or any Employment Agency nor we guarantee any employment. We do not ask candidates for any fees, Personal Information like (Bank OTP, Credit-Debit Card No, Aadhar Card OTP etc.) Please be Aware And never Share Such Information to any one or In the Name of agrijob.in. Please verify the correctness of the Agri jobs details yourself. We do not offer any guarantee on correctness of any details mentioned here. If a candidate pays any amount to anyone claiming to represent any company then it would be the responsibility of that candidate and he cannot hold us or the concerned employer responsible for such fraudulent activities.