Agricultural Land Mortgage India 2026 – NRI Investor’s Complete Legal Guide

Agricultural Land Mortgage India 2026 is one of the most searched legal topics among Non-Resident Indians (NRIs) and Overseas Citizens of India (OCIs) looking to manage, leverage, or invest in farmland back home. Whether you inherited agricultural land, received it as a gift, or hold it from before you became an NRI, understanding the legal framework of agricultural land mortgage in India is essential before approaching any bank or legal adviser. This comprehensive guide covers FEMA restrictions, the six types of mortgages under the Transfer of Property Act 1882, bank loan rates for 2026, SARFAESI applicability, stamp duty, tax implications, and repatriation rules — making it indispensable for NRI investors and international agriculture graduates considering India vs USA investment comparisons. Read on for complete details and visit agrijob.in for the latest updates.

Table of Contents

Agricultural Land Mortgage India 2026 – Quick Overview

| Parameter | Details |

|---|---|

| Governing Law | Transfer of Property Act, 1882 (Sections 58–104); FEMA 1999; NDI Rules 2019; SARFAESI Act, 2002 |

| Regulatory Authority | Reserve Bank of India (RBI), Ministry of Finance |

| NRI Purchase Status | PROHIBITED (Rule 24, FEMA NDI Rules 2019) |

| NRI Ownership Routes | Inheritance, Gift from resident relative, Pre-NRI holding, RBI special approval (rare) |

| Mortgage Types | 6 types under Sec 58 TPA: Simple, Usufructuary, Conditional Sale, English, Equitable (Deposit of Title Deeds), Anomalous |

| Bank Loan LTV | Up to 75% of market value (SBI, NABARD, RRBs) |

| Interest Rate Range | 7.0%–10.5% p.a. (2025–26) |

| Repayment Period | Up to 10–20 years (bank-specific) |

| SARFAESI Applicability | NOT applicable to pure agricultural land (Sec 31(i), SARFAESI Act) |

| FEMA Violation Penalty | Up to 3× purchase price (Delhi HC, 2024) |

| Repatriation Cap | USD 1 million per financial year (NRO account) |

| Capital Gains Tax (LTCG) | 12.5% without indexation (for urban agri land held >2 years) |

| Official Website | rbi.org.in |

Can NRIs Buy or Mortgage Agricultural Land in India? FEMA Position 2026

The starting point for any agricultural land mortgage India 2026 discussion must be the FEMA prohibition on NRI purchase. Under Rule 24 of the Foreign Exchange Management (Non-Debt Instruments) Rules, 2019, an NRI or OCI card holder cannot acquire agricultural land, plantation property, or a farmhouse in India by way of purchase. This is not an administrative guideline — it is a statutory restriction enforced by the RBI, and banks or sellers cannot waive it.

The underlying provision is Section 6(5) of FEMA, 1999, which states that a person resident outside India who is an Indian citizen (NRI) or Person of Indian Origin (PIO) cannot acquire agricultural land, plantation property, or a farmhouse in India except through inheritance. The RBI holds residual discretionary power under Section 6(3)(i) of FEMA 1999, read with Rule 7 of the NDI Rules, to grant special prior approval on a case-by-case basis — but in practice this is extremely rare and not a route for routine investment planning.

Critical FEMA penalty (2024 Delhi High Court case): An OCI cardholder bought agricultural land in Tamil Nadu for ₹13.68 lakh. The RBI directed sale, the OCI complied — but the RBI still imposed a compounding penalty of ₹41.04 lakh (exactly 3× the acquisition price). The Delhi High Court in 2024 dismissed his petition. This real case makes clear that cooperation after the fact does not erase the violation. The penalty can be up to three times the amount involved.

Legal Routes for NRI Agricultural Land Ownership in India

| Route | Legal Basis | Conditions | Can Mortgage? |

|---|---|---|---|

| Inheritance | Section 6(5) FEMA 1999 | From resident Indian relative; can retain or sell to resident Indian only | Yes — with bank approval |

| Gift from Resident Relative | FEMA NDI Rules 2019 | Donor must be FEMA-defined relative (Sec 2(77), Companies Act 2013); NRI→NRI gift not allowed | Yes — with bank approval |

| Pre-NRI Holding | Section 6(4) FEMA 1999 | Land acquired when individual was resident in India; can continue to hold after becoming NRI | Yes — subject to state law |

| Special RBI Approval | Section 6(3)(i), Rule 7 NDI Rules | Exceptional cases only; must show genuine agri or public welfare purpose; apply to CGM RBI Mumbai | Yes — if approval granted |

Once an NRI legitimately holds agricultural land through any of the above routes, the question of mortgage becomes relevant. The NRI can approach Indian banks to raise a loan against this agricultural land — but eligibility, documentation, and terms differ significantly from resident Indian borrowers.

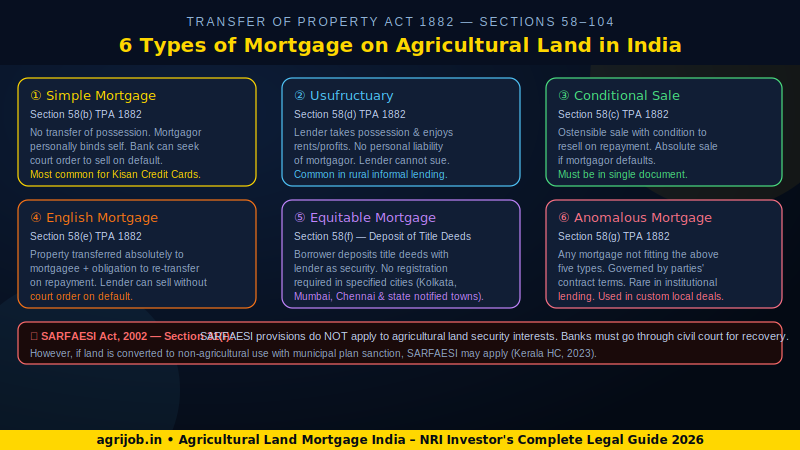

Agricultural Land Mortgage India 2026 – 6 Types Under Transfer of Property Act 1882

Under Sections 58–104 of the Transfer of Property Act, 1882 (TPA), there are six legally recognised types of mortgage applicable to agricultural land in India. Every bank loan or private mortgage against farmland falls into one of these categories.

| # | Mortgage Type | Section (TPA 1882) | Key Feature | Common Use |

|---|---|---|---|---|

| 1 | Simple Mortgage | Section 58(b) | No transfer of possession. Mortgagor personally bound. Lender gets court order to sell on default. | Kisan Credit Card, crop loans, NABARD refinanced loans |

| 2 | Mortgage by Conditional Sale | Section 58(c) | Ostensible sale with condition — sale becomes absolute on default; becomes void on repayment. Must be in a single document. | Private lenders, rural informal credit markets |

| 3 | Usufructuary Mortgage | Section 58(d) | Lender takes possession and enjoys rents/profits. No personal liability of mortgagor. No right to sue or foreclose. | Traditional rural lending; community-based credit arrangements |

| 4 | English Mortgage | Section 58(e) | Absolute transfer to mortgagee + obligation to re-transfer on repayment. Lender can sell without court on default. | Institutional lenders in major cities; commercial properties |

| 5 | Mortgage by Deposit of Title Deeds (Equitable Mortgage) | Section 58(f) | Borrower deposits title deeds with lender as security. No registration required in notified cities (Mumbai, Kolkata, Chennai, and state-notified towns). | SBI, HDFC, ICICI — urban & semi-urban loans; faster processing |

| 6 | Anomalous Mortgage | Section 58(g) | Any mortgage not covered by types 1–5. Governed by contract terms between parties. | Rare; custom private transactions; local agricultural cooperatives |

For NRIs holding agricultural land through inheritance or gift, the Simple Mortgage and Equitable Mortgage (Deposit of Title Deeds) are the two types most commonly accepted by Indian scheduled banks. The Simple Mortgage requires formal registration with the Sub-Registrar; the Equitable Mortgage requires deposit of original title deeds and can be created without registration in notified cities, making it faster and cheaper.

SARFAESI Act 2002 and Agricultural Land — What NRIs Must Know

The Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002 (SARFAESI) allows banks to enforce security interests without court intervention. However, Section 31(i) of SARFAESI explicitly excludes agricultural land from its provisions. This means if you mortgage agricultural land to a bank and default, the bank cannot directly auction or take possession under SARFAESI — it must approach the civil court or Debt Recovery Tribunal (DRT).

The Kerala High Court (October 2023) clarified that the question of whether a mortgaged property is truly agricultural or not — a key factual question — must be decided by the DRT and cannot be challenged through a writ petition. However, if a municipality has sanctioned a building plan on agricultural land (converting its use), SARFAESI provisions may apply. This is a critical nuance for NRIs holding inherited farmland in peri-urban areas where land use conversion has occurred.

Application Fee for Mortgage Registration

| Fee Type | Amount | Notes |

|---|---|---|

| Stamp Duty on Mortgage Deed | 0.1%–0.5% of loan amount (state-specific) | Varies by state; Maharashtra, UP, Karnataka have different slab rates |

| Registration Fee (Sub-Registrar) | ₹500–₹10,000 (state-specific caps) | Required for Simple, Conditional Sale, and English mortgage; not for Equitable Mortgage |

| Bank Processing Fee | 0.5%–1% of loan amount | SBI, NABARD — typically 0.5%; some banks waive for Kisan loans |

| Valuation / Inspection Fee | ₹1,000–₹5,000 | Independent surveyor appointed by bank; satellite-based valuation increasingly used in 2025–26 |

| Legal / Documentation Charges | ₹2,000–₹10,000 | Mortgage deed drafting, title search, encumbrance certificate |

Agricultural Land Mortgage India 2026 – Bank Loan Rates & EMI Comparison

For NRIs or resident Indians holding clear-title agricultural land, several major Indian banks offer loans against this security. Here is a current comparison for agricultural land mortgage India 2026:

| Bank | Max LTV | Interest Rate (p.a.) | Max Repayment | Key Condition |

|---|---|---|---|---|

| SBI (Asset-Backed Agri Loan) | Up to 75% | 7.2%–9.5% | 10 years | Primary security: hypothecation of assets; collateral: SARFAESI-compliant property |

| NABARD (via RRBs) | Up to 70% | 7.0%–9.0% | 7–15 years | Farmers, SHGs, FPOs; long-term investment credit via RIDF |

| HDFC Bank | Up to 50% | 9.0%–10.5% | 20 years | Flexible repayment; NRI co-applicant allowed on residential; agri land on case basis |

| Axis Bank | Up to 60% | 9.5%–10.5% | 15 years | Crop cycle-aligned repayment; quarterly/half-yearly EMI options |

| Union Bank of India | Up to 65% | 7.5%–9.5% | 10 years | Priority sector lending; Kisan Credit Card integration available |

| Regional Rural Banks (RRBs) | Up to 60% | 7.0%–8.5% | 7 years | State-specific; sponsored by NABARD; best rates for small & marginal farmers |

Interest rate note (2025–26): Standard agricultural land mortgage interest rates range from 7.2% to 10.5% per annum, with further reductions available under government interest subvention schemes. Repayment schedules can be structured to align with crop cycles — quarterly, half-yearly, or annual instalments based on farm cash flow. Prepayment charges are nil or minimal for floating-rate loans. Processing fees are typically 0.5%–1% of the loan amount.

Eligibility and Documentation for NRI Agricultural Land Mortgage

- Clear, marketable title to agricultural land in India — verified through title deed, Khasra/Khatauni/Jamabandi records, and encumbrance certificate (EC) from Sub-Registrar

- Valid land record documents: certified copy of title deed, mutation certificate, latest land tax payment receipt, survey map

- Proof of NRI status and legitimate ownership route: inheritance certificate / succession certificate / gift deed registered under the Registration Act, 1908

- Identity documents: Passport (mandatory), PAN card (mandatory for all India tax compliance), OCI/PIO card, Aadhaar (where applicable)

- NRE/NRO bank account: loan disbursement and repayment must flow through Indian banking channels in INR

- Power of Attorney (PoA): if NRI is not present in India, a notarised and apostilled PoA to an Indian resident is required for executing mortgage deed and interacting with the Sub-Registrar

- Income proof / creditworthiness: overseas salary slips, employment contract, ITR (if Indian income exists), CIBIL/CRIF credit score above 650 preferred

- FEMA compliance certificate: bank’s legal team will verify the NRI’s title acquisition was through an approved route (inheritance/gift) — not a direct purchase

- No-dues certificate: confirming land is free of any prior mortgage, charge, or lien

- Two valuation reports for loans above ₹1 crore (SBI requirement, 2025)

Tax Implications for NRI Agricultural Land Mortgage and Sale in India 2026

| Transaction | Tax Type | Rate (2025–26) | Notes |

|---|---|---|---|

| Sale of rural agricultural land | Capital Gains | NIL | Rural agri land is NOT a capital asset under Income Tax Act; no CGT applies |

| Sale of urban agricultural land (held >2 years) | LTCG | 12.5% (no indexation) | Urban agri land defined as per Section 2(14)(iii) — within municipality / 8 km radius |

| Sale of urban agricultural land (held ≤2 years) | STCG | Slab rate (30% + surcharge for NRIs) | Added to total income; TDS deducted by buyer before payment |

| TDS on NRI sale proceeds | TDS | 20% LTCG / 30% STCG + surcharge + 4% cess | Buyer must deduct before paying NRI; Form 16B issued |

| DTAA benefit | Tax Treaty | Lower rate per treaty | NRIs from USA, UK, UAE, Canada, Australia etc. — check India DTAA; may reduce TDS obligation |

| Repatriation of sale proceeds | RBI/FEMA | USD 1 million/year cap | Must be credited to NRO account first; repatriation requires CA certificate Form 15CA/15CB |

| Rental income from mortgaged land | Income Tax | Slab rate | 30% standard deduction on rental income; TDS 30% by tenant if NRI |

Step-by-Step Process to Mortgage Agricultural Land in India as an NRI

- Verify ownership legitimacy: Confirm your land was acquired through inheritance, gift from a resident relative, or is a pre-NRI holding. Obtain certified copies of inheritance/succession certificate or registered gift deed.

- Get title search and EC: Commission a lawyer or empanelled bank advocate to conduct a title search and obtain an Encumbrance Certificate (EC) for the last 30 years from the Sub-Registrar’s office.

- Arrange PoA: If you are abroad, execute a notarised and apostilled Power of Attorney in favour of a trusted resident Indian to act on your behalf for mortgage creation and bank dealings.

- Approach the bank: Contact SBI, NABARD-linked RRB, Union Bank of India, or your state cooperative bank. Submit the loan application with land documents, identity proof, income documents, and FEMA compliance evidence.

- Land valuation: Bank appoints an independent valuer. Loan sanctioned up to 60–75% of assessed market value depending on the bank and state.

- Mortgage deed drafting: Bank’s legal team or your advocate drafts the mortgage deed. Most institutional loans use Simple Mortgage or Equitable Mortgage (Deposit of Title Deeds) for speed.

- Stamp duty payment and registration: Pay applicable stamp duty (0.1%–0.5%) on the mortgage deed. For Simple Mortgage: register with Sub-Registrar (mandatory). For Equitable Mortgage: deposit original title deeds with bank (no registration needed in notified cities).

- Loan disbursement: Funds credited to your NRO/NRE account or directly to the designated purpose (purchase of agri inputs, machinery, etc.) as per sanction terms.

- Repayment: Repay through NRE/NRO account via NEFT/RTGS. Align repayment schedule with crop cycle for convenience — discuss quarterly or half-yearly options with your branch.

- Redemption: On full repayment, exercise Right of Redemption under Section 60 TPA 1882. Bank returns title deeds and executes release deed. Get registered release of mortgage at Sub-Registrar.

Agricultural Land Mortgage India 2026 — NRI vs Resident Indian: Key Differences

| Factor | Resident Indian | NRI (FEMA-compliant holding) |

|---|---|---|

| Purchase of agricultural land | ✅ Permitted (subject to state laws) | ❌ Prohibited (FEMA NDI Rule 24) |

| Mortgage of agricultural land | ✅ Freely permitted | ✅ Permitted if land held via legal route |

| Bank loan against agricultural land | ✅ All scheduled banks | ✅ Subject to FEMA compliance documentation |

| Loan repayment account | Regular savings/current account | Must use NRE or NRO account (INR) |

| TDS on sale | 1% if >₹50 lakh (Sec 194-IA) | 20–30% + surcharge + cess (Sec 195) |

| Repatriation of sale proceeds | No restriction | USD 1 million/year cap; Form 15CA/15CB |

| SARFAESI recovery by bank | Not applicable (agri land exempt) | Not applicable (agri land exempt) |

| Capital gains on rural agri land sale | NIL (not a capital asset) | NIL (same) |

| Power of Attorney required | Optional | Required if abroad |

Agricultural Land Mortgage India vs USA — NRI Investment Perspective 2026

For NRIs and international agriculture graduates comparing agricultural land mortgage India 2026 with equivalent instruments abroad, the differences are stark. In the USA, a farm mortgage (agricultural real estate loan) through the Farm Credit System or USDA Farm Service Agency offers rates between 6.5%–8.5% p.a. for 2026 — but land prices are dramatically higher ($5,000–$12,000 per acre in the Midwest vs ₹5–50 lakh per acre in India depending on state and location).

For NRIs returning to India who wish to reinvest remittances in the agricultural sector, the legal complexity of FEMA restrictions on direct purchase — combined with the opportunity to receive inherited or gifted land — creates a unique investment scenario. The mortgage route allows NRIs to unlock liquidity from inherited farmland without selling it. This is particularly valuable for NRI families in states like Punjab, Haryana, Maharashtra, Karnataka, and Kerala where land values have appreciated 3–5× over the last decade.

For international agriculture students from Indian origin currently studying in the USA, UK, Canada, or Australia: if you anticipate inheriting agricultural land in India, it is advisable to understand the mortgage framework now. Eligible NRIs living abroad can manage Indian agricultural land through a trusted PoA holder, service a bank loan through NRO accounts, and potentially generate rental or crop-sharing income while abroad — creating a passive income stream in INR without violating FEMA regulations.

The India vs USA comparison for agricultural land investment in 2026: India offers far higher yield-on-cost due to lower land prices, significant government agri support schemes (PM-KUSUM, PM-KISAN, Soil Health Card), and NABARD credit at rates subsidised below market. NRIs who hold land legitimately should consider it a long-term asset and explore institutional credit against it rather than distress sale.

State-Wise Stamp Duty on Agricultural Land Mortgage Deed (2025–26)

| State | Stamp Duty on Mortgage Deed | Registration Fee | Notes |

|---|---|---|---|

| Maharashtra | 0.1% (max ₹10 lakh) | ₹30,000 cap | Equitable mortgage: no registration, 0.3% stamp on MoD letter |

| Uttar Pradesh | 0.5% of loan | 0.1% of loan | Higher rates for urban areas |

| Rajasthan | 0.5% (max ₹25,000) | ₹500–₹5,000 | Concession for Kisan Credit Card-linked mortgages |

| Karnataka | 0.5% of loan | 0.5% of loan | Kaveri online portal for EC and encumbrance search |

| Punjab / Haryana | 0.5%–1% of loan | ₹1,000–₹5,000 | NRI-heavy states; check district-specific collector rates |

| Bihar | 1% of loan | 0.1% of loan | BREDA portal for state agri scheme integration |

| Tamil Nadu | 1% of loan (max ₹40,000) | ₹60,000 cap | Kaveri equivalent: EC via Registration Dept portal |

| Gujarat | 0.5% of loan | 0.5% of loan | GEDA integration with agri loan schemes |

Important Links

| Resource | Link |

|---|---|

| RBI — FEMA FAQs (Immovable Property) | rbi.org.in — FEMA FAQ |

| FEMA NDI Rules 2019 (official) | RBI Official Website |

| Transfer of Property Act 1882 — Section 58 (Indiankanoon) | Section 58 TPA — Indiankanoon |

| SBI Asset-Backed Agri Loan | SBI Agri Loan |

| NABARD Long Term Loans | nabard.org |

| More Agriculture & NRI Scheme News | Latest Agriculture Jobs & Schemes |

| Latest Govt Jobs 2026 | Govt Jobs 2026 |

| Join Telegram for Alerts | agrijob.in Telegram Channel |

Frequently Asked Questions about Agricultural Land Mortgage India 2026

Q1. What is agricultural land mortgage India 2026 and can NRIs do it?

Agricultural land mortgage India 2026 refers to creating a charge on farmland as security for a bank loan under Sections 58–104 of the Transfer of Property Act, 1882. NRIs can mortgage agricultural land they hold legitimately (through inheritance, gift, or pre-NRI purchase) but cannot buy agricultural land directly under FEMA. The mortgage itself is legally valid if the underlying ownership is FEMA-compliant.

Q2. Can an NRI mortgage inherited agricultural land to get a bank loan in India?

Yes. An NRI who has inherited agricultural land from a resident Indian relative can mortgage it to an Indian bank (SBI, NABARD, RRBs, etc.) to obtain a loan. The bank will verify FEMA compliance, conduct a title search, and typically lend up to 60–75% of the market value. Repayment must be through NRE/NRO accounts.

Q3. What are the six types of mortgage on agricultural land under Indian law?

Under Section 58 of the Transfer of Property Act 1882, the six types are: (1) Simple Mortgage, (2) Mortgage by Conditional Sale, (3) Usufructuary Mortgage, (4) English Mortgage, (5) Mortgage by Deposit of Title Deeds (Equitable Mortgage), and (6) Anomalous Mortgage. Banks primarily use Simple Mortgage and Equitable Mortgage for institutional agricultural land loans.

Q4. Does SARFAESI Act apply to agricultural land in India?

No. Section 31(i) of the SARFAESI Act, 2002 explicitly excludes security interests created in agricultural land from SARFAESI provisions. Banks cannot directly auction or take possession of agricultural land under SARFAESI on default — they must go through civil court or DRT. However, if the land has been converted to non-agricultural use with municipal sanction, SARFAESI may apply.

Q5. What is the penalty for an NRI who illegally buys agricultural land in India?

The FEMA penalty is up to three times the purchase price of the agricultural land. In a 2024 Delhi High Court case, an OCI who bought agricultural land for ₹13.68 lakh was penalised ₹41.04 lakh (3×) even after cooperating with the RBI and selling the land. FEMA violations are civil, not criminal, but the financial penalty is severe.

Q6. Can NRIs or Indian students abroad invest in Indian agricultural land indirectly?

Yes. NRIs cannot buy agricultural land directly, but they can (a) inherit it, (b) receive it as a gift from a FEMA-defined resident relative, and (c) invest in agri-related companies, REITs with agricultural exposure, or agritech startups that own or lease farmland. For NRIs in USA, UK, or Canada, investing in India’s agricultural sector through commodity trading, FPO (Farmer Producer Organisation) equity, or agribusiness loans is also possible within FEMA guidelines.

Final Thoughts on Agricultural Land Mortgage India 2026

Agricultural Land Mortgage India 2026 is a legally nuanced but entirely viable strategy for NRIs who hold farmland through legitimate routes under FEMA. The six mortgage types under the Transfer of Property Act 1882 offer flexibility — from the court-backed Simple Mortgage favoured by institutional lenders to the faster Equitable Mortgage via deposit of title deeds. With bank interest rates ranging from 7%–10.5% p.a. and LTV ratios up to 75%, NRI landholders can unlock substantial liquidity without selling inherited farmland. The key safeguards are FEMA compliance, correct documentation, proper PoA arrangements if abroad, and awareness of SARFAESI’s non-applicability to agricultural security. Never attempt to purchase agricultural land directly as an NRI — the 3× penalty is real, as confirmed by the 2024 Delhi High Court judgement. Consult a FEMA-specialist property lawyer and CA before any transaction. Visit agrijob.in for more agriculture law updates, government scheme guides, and NRI investment news in India.

Disclaimer: This Agricultural jobs related information is only for the purpose of providing information to you and for Agricultural career advancement of Agricultural, Horticulture, Agronomy, Soil Science, Plant Breeding, Agriculture Marketing, Forestry, Poultry, Fisheries, Agri Business Management Graduates. We are not representing this employer or any Employment Agency nor we guarantee any employment. We do not ask candidates for any fees, Personal Information like (Bank OTP, Credit-Debit Card No, Aadhar Card OTP etc.) Please be Aware And never Share Such Information to any one or In the Name of agrijob.in. Please verify the correctness of the Agri jobs details yourself. We do not offer any guarantee on correctness of any details mentioned here. If a candidate pays any amount to anyone claiming to represent any company then it would be the responsibility of that candidate and he cannot hold us or the concerned employer responsible for such fraudulent activities.UPCATET 2023 Entrance What is UPCATET Entrance – जाने क्या है कौन छात्र छात्रा दे सकते है , क्या फायदा हो सकता है |CUET 2023 ENTRANCE EXAM