Agri-NBFCs in India 2026 – Best Non-Banking Lenders for Farm Businesses Compared

Agri-NBFCs in India 2026 are rapidly transforming how farmers, Farmer Producer Organisations (FPOs), agri-MSMEs, and rural entrepreneurs access credit. As India’s agriculture sector evolves into a structured value chain in 2026, Non-Banking Financial Companies (NBFCs) regulated by the Reserve Bank of India (RBI) are filling a critical gap that traditional banks often cannot — fast disbursals, flexible collateral, and farmer-friendly loan products tailored to seasonal income cycles. This complete guide compares the best Agri-NBFCs in India 2026, covering their loan products, interest rates, eligibility, and how to apply. Read on for complete details and apply via agrijob.in.

Table of Contents

Agri-NBFCs in India 2026 – Quick Overview

| Detail | Information |

|---|---|

| Regulator | Reserve Bank of India (RBI) — rbi.org.in |

| Refinancing Body | NABARD — National Bank for Agriculture & Rural Development |

| Policy Framework | RBI Scale-Based Regulation (SBR) for NBFCs — 2022 onwards |

| Interest Rate Range | 12% – 22% p.a. (varies by NBFC, loan type & borrower profile) |

| Typical Loan Size | ₹10,000 – ₹50 Crore (varies by NBFC) |

| Eligible Borrowers | Farmers, SHGs, JLGs, FPOs, Agri-MSMEs, Agri Startups |

| Disbursal Speed | 3 – 15 Working Days (faster than traditional banks) |

| Collateral | Gold, Warehouse Receipt, Land, or Collateral-Free (product-specific) |

| Application Mode | Online / App / Branch / Business Correspondent |

| Official Source | rbi.org.in |

What Are Agri-NBFCs? Why Do They Matter in 2026?

A Non-Banking Financial Company (NBFC) is a company registered under the Companies Act and regulated by the RBI that provides loans, advances, and financial services — but without a full banking licence. Agri-NBFCs are NBFCs that specifically focus on the agricultural sector, rural lending, and allied farm activities.

According to the RBI’s official FAQ on NBFCs (updated April 2026), NBFCs are engaged in the business of loans and advances, acquisition of shares, bonds, and securities, but unlike banks, they cannot accept demand deposits or issue cheques. This makes them highly focused, agile lenders who can design custom products for the farm sector.

In 2026, Agri-NBFCs in India are moving from simple crop-financing to full value-chain financing — covering production, post-harvest storage, commodity trading, food processing, and even agri-tech startups. The Government of India’s Agriculture Infrastructure Fund (AIF) portal at agriinfra.dac.gov.in has also listed NBFCs as eligible lending institutions, further validating their role in the national agri-finance ecosystem.

Agri-NBFCs in India 2026 – Top 8 Compared

Here is a detailed comparison of the best Agri-NBFCs in India 2026, sourced from official RBI registrations, NABARD subsidiary data, and company disclosures:

| # | NBFC Name | Promoter / Parent | Focus Area | Loan Products | Interest Rate | Best For |

|---|---|---|---|---|---|---|

| 1 | NABKISAN Finance Ltd (NKFL) | NABARD Subsidiary | FPOs, SHGs, JLGs, Rural MSMEs | FPO Loans, MFI Lending, Agri Value Chain | ~10%–14% p.a. | FPOs & PACS |

| 2 | NABSamruddhi Finance Ltd | NABARD Subsidiary | Off-Farm, Agro Processing, SHGs | Bulk Lending to NBFCs/MFIs, PTC Investment | ~10%–13% p.a. | NBFCs & MFIs on-lending |

| 3 | Kissandhan Agri Financial Services | SLCM Group (RBI Regulated) | Commodity Finance, FPOs, Agri MSMEs | Commodity-Based Loans, FPO Finance, Invoice Discounting, Jansamridhi Loan | ~14%–18% p.a. | Commodity traders & FPOs |

| 4 | Samunnati Financial Services | Private / VC-Backed NBFC | Agri Value Chain — Full Spectrum | SME Agri Loans, FPO Finance, Agri Enterprise Loans | ~14%–20% p.a. | Agri SMEs & FPOs |

| 5 | NAFA (Netafim Agricultural Financing Agency) | Netafim Group (RBI Licence 2013) | Micro-Irrigation Finance | Drip & Sprinkler Irrigation Equipment Loans | ~12%–16% p.a. | Irrigation equipment buyers |

| 6 | Jai Kisan (Bharat Agri Fincorp) | Private Fintech NBFC | Small Farmers, Agri Inputs | Input Finance, Farm Equipment, Working Capital | ~16%–22% p.a. | Small farmers & input dealers |

| 7 | Avanti Finance | Private NBFC (RBI Registered) | Rural Microfinance & Agri Credit | JLG Loans, Rural Enterprise Finance | ~18%–22% p.a. | Marginal farmers & rural women |

| 8 | AU Small Finance Bank (Agri Division) | Small Finance Bank (SFB) | Agri Business & Kisan Loans | Kisan Loan, Tractor Loan, Agri Term Loan | ~12%–18% p.a. | Agri businesses & tractor buyers |

NABKISAN Finance Limited – Government-Backed NBFC for FPOs

NABKISAN Finance Limited (NKFL), formerly known as Agri Development Finance (Tamil Nadu) Limited, is one of the most trusted Agri-NBFCs in India 2026. It is a wholly owned subsidiary of NABARD, incorporated on 14 February 1997, and is notified as an NBFC by the RBI.

NABKISAN’s primary objective is to provide credit for the promotion, expansion, and commercialisation of enterprises in agriculture, allied activities, and rural non-farm sectors. In its bulk lending segment, NABKISAN focuses on lending to NBFCs in rural areas, FPOs, agri-MSMEs, and value chain participants. It works with NCDEX, SEBI, NCDEX e-Markets Limited, and various state governments to provide FPO loans at concessional interest rates.

Best For: Farmer Producer Organisations (FPOs), PACS, Panchayat Level Federations, MFIs, and agri-tech startups. Official website: nabkisan.org

NABSamruddhi Finance Limited – NABARD Subsidiary for Off-Farm Activities

NABSamruddhi Finance Limited is another NABARD subsidiary NBFC that provides long-term finance to NBFCs and NBFC-MFIs for on-lending to corporates, individuals, Producer Companies, Federations, Trusts, Societies, Section 8 Companies, SHGs, and JLGs for off-farm and secondary agricultural activities.

NABSamruddhi’s Pooled Loan Issuance (PLI) is a unique structured product that provides loans to multiple small and mid-sized NBFCs — all backed by a common partial guarantee. This helps NBFCs serving vulnerable borrowers access institutional liquidity. NABSamruddhi has also invested in Pass Through Certificates (PTCs) involving underlying pools of off-farm loans from partner NBFCs.

Best For: NBFCs and MFIs seeking refinance, agro-processing units, WASH (Water, Sanitation & Hygiene) finance, and producer collectives. Official: nabsamruddhi.in

Kissandhan Agri Financial Services – Multi-Asset Agri NBFC

Kissandhan Agri Financial Services Private Limited is one of the leading RBI-regulated Agri-NBFCs in India 2026. A wholly-owned subsidiary of the SLCM (Sohan Lal Commodity Management) Group, Kissandhan has disbursed over ₹35 Billion to date, impacting approximately half a million farmers, agri-processors, and agri traders across India.

Kissandhan’s flagship product — Commodity-Based Financing (CBF) — is unique: the underlying agricultural commodity held in a scientific warehouse is the primary collateral, allowing farmers and agri-traders to access credit without selling their produce at distress prices. Other key products include FPO Finance, Lending to NBFC-MFIs for JLG on-lending, Invoice Bill Discounting for Agri-MSMEs, and the Jansamridhi Loan (property-backed loan for rural borrowers).

Key Advantages: Hassle-free documentation, phygital lending (online + offline), fast disbursal, and deep expertise in agri commodity ecosystems. Official: kissandhan.com

Samunnati Financial Services – India’s Largest Agri Value Chain Financer

Samunnati Financial Intermediation and Services Pvt Ltd is a Chennai-based NBFC that is India’s largest agriculture value chain finance institution. Founded in November 2014 and backed by Accel, Elevar Equity, and other institutional investors, Samunnati lends to the entire spectrum of agriculture players — from small retail farmers to larger agri-SME borrowers.

What sets Samunnati apart among Agri-NBFCs in India 2026 is its value-chain approach: rather than financing just one player, Samunnati finances aggregators, processors, and market intermediaries throughout a specific commodity’s value chain, improving repayment capacity across the board. It works with over 65 community-based organisations and 35 agri enterprises, and extends financial services to their members.

Best For: Agri-SMEs, FPOs seeking market linkages, banana/cotton/paddy/oilseed value chains, and agri-enterprises seeking both finance and advisory services. Official: samunnati.com

NAFA – Micro-Irrigation Focused Agri NBFC

Netafim Agricultural Financing Agency Pvt Ltd (NAFA) is an RBI-licensed NBFC that began operations in March 2013. NAFA was founded specifically to solve a critical bottleneck: farmers who wanted to adopt micro-irrigation (drip and sprinkler systems) lacked access to affordable finance.

NAFA provides customised financial solutions to the entire smart irrigation value chain — from individual farmers buying drip systems to irrigation dealers and distributors. As one of the more specialised Agri-NBFCs in India 2026, NAFA is a strong choice for farmers wanting to upgrade to water-efficient farming, particularly in water-stressed regions of Maharashtra, Gujarat, Karnataka, and Andhra Pradesh. Official: nafa.co.in

Eligibility to Apply at Agri-NBFCs in India 2026

- Individual Farmers: Small, marginal, and large farmers directly engaged in crop production, horticulture, animal husbandry, fisheries, or other allied activities.

- Self Help Groups (SHGs): Women and mixed SHGs engaged in farming or agro-processing at village level.

- Joint Liability Groups (JLGs): Groups of 4–10 farmers who jointly guarantee each other’s loans — popular for collateral-free agri credit.

- Farmer Producer Organisations (FPOs/FPCs): Producer companies, cooperatives, and registered FPOs can access institutional credit at concessional rates from NABKISAN and Samunnati.

- Agri-MSMEs: Food processing units, agri-input dealers, cold chain operators, agro-warehousing companies, and agri-service providers.

- Agri Startups: NABKISAN explicitly offers innovative financing for agricultural technology startups and entrepreneurs.

- NRI-Linked Agri Businesses: Agri-businesses promoted by NRIs returning to India, or co-promoted with Indian resident partners, are eligible at most NBFCs subject to FEMA and RBI norms (see NRI section below).

Documents Required

- KYC: Aadhaar, PAN, Voter ID, or any RBI-approved identity and address proof

- Income Proof: Bank statements (6 months), income tax returns (if applicable), or crop production records

- Land Records: 7/12 extract, ROR, or land lease agreement (for land-linked loans)

- Commodity Documents: Warehouse receipt, quality certificate, WDRA registration (for commodity-backed loans)

- FPO Documents: Certificate of Incorporation, Board Resolution, member list, audited financials (for FPO loans)

- Business Plan: For agri-MSMEs and startups — project report with financial projections

- Photographs: Recent passport-size photographs

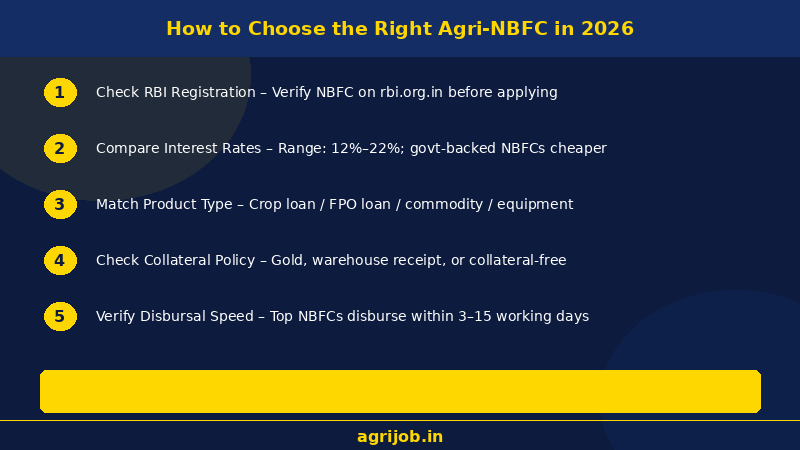

How to Apply at Agri-NBFCs in India 2026

- Verify RBI Registration: Always confirm the NBFC is listed on the RBI’s official NBFC register at rbi.org.in before applying. This is the single most important step to avoid fraudulent lenders.

- Identify the Right Product: Match your need — crop loan (Kissandhan), FPO loan (NABKISAN), irrigation equipment (NAFA), agri-enterprise loan (Samunnati), or rural microfinance (Avanti Finance).

- Contact the NBFC: Visit the NBFC’s official website or nearest branch / Business Correspondent (BC) in your district. Most top NBFCs offer an online enquiry form or a dedicated toll-free number.

- Submit Application & Documents: Complete the loan application form and submit KYC + relevant financial and land documents. Kissandhan follows a minimised documentation process; commodity-backed loans additionally require warehouse receipts.

- Field Visit / Virtual Assessment: The NBFC’s loan officer may visit for a field assessment or conduct a virtual verification using satellite-based crop monitoring tools in some cases.

- Loan Sanction: Top Agri-NBFCs sanction loans in 3–15 working days — significantly faster than traditional banks.

- Disbursement: Funds are credited to your bank account (NEFT/RTGS) or disbursed through a Business Correspondent. Commodity loans may be disbursed against electronic warehouse receipts.

Agri-NBFCs vs Traditional Banks – Which is Better in 2026?

| Parameter | Traditional Banks (PSBs/SCBs) | Agri-NBFCs in India 2026 |

|---|---|---|

| Interest Rate | 7%–10% p.a. (subsidised) | 12%–22% p.a. (market-linked) |

| Disbursal Speed | 15–60 days | 3–15 days |

| Collateral Flexibility | Usually land/property required | Gold, commodity, or collateral-free |

| Product Customisation | Standardised products | Highly customised, value-chain linked |

| Documentation | Extensive | Minimal to moderate |

| Rural Reach | Limited in remote areas | Deep rural reach via BCs & phygital model |

| FPO / Agri Startup Loans | Limited | Core strength of top Agri-NBFCs |

| Interest Subvention | Available (2–3% discount for prompt repayment) | Generally not available |

| CIBIL Requirement | Strict CIBIL score requirement | More flexible, especially for new borrowers |

| Best Use Case | Large loans, long-term farm development | Working capital, FPO finance, value chain credit |

Verdict: For small farmers needing crop loans or land development finance, traditional banks remain cheaper thanks to government interest subvention. But for FPOs, agri-MSMEs, commodity traders, and agri-startups who need fast credit with flexible collateral, Agri-NBFCs in India 2026 are the clear winner.

RBI Regulatory Framework for Agri-NBFCs in 2026

All legitimate Agri-NBFCs in India 2026 are regulated by the Reserve Bank of India under the RBI Act, 1934, and the Non-Banking Financial Companies – Registration, Exemptions and Framework for Scale Based Regulation (SBR). According to the RBI’s latest NBFC FAQ (updated April 29, 2026), NBFCs must be registered under the Companies Act 1956 or 2013 and must pass the “50-50 test” — where financial business constitutes more than 50% of total assets or income.

Key protections for borrowers at RBI-registered NBFCs include transparent disclosure of interest rates and all charges in the application form and the Key Facts Statement (KFS), a mandatory loan card for microfinance borrowers in a language they understand, and no requirement for deposit/margin/collateral for microfinance loans. Always verify an NBFC on the RBI’s official portal before applying.

Is Borrowing from Agri-NBFCs a Good Option for NRIs and International Agriculture Graduates?

For NRIs returning to India and international agriculture graduates looking to set up farm businesses, Agri-NBFCs in India 2026 offer some distinct advantages over traditional banks. The faster processing, flexible collateral policies, and customised agri-enterprise loan products make them well-suited for new farm businesses that may not have years of documented farm income history.

In an India vs USA comparison, American USDA farm loans require US residency and domestic credit history. In contrast, Indian Agri-NBFCs are increasingly accepting alternative credit assessments — digital transaction records, FPO membership history, or satellite-verified farm activity — making them accessible to returning NRIs who lack traditional collateral in India. Several for international students who return to India with degrees in Agribusiness Management, Agricultural Finance, or Precision Farming, NBFCs like NABKISAN and Samunnati explicitly finance agri-tech startups and innovative farming ventures.

The Agriculture Infrastructure Fund (AIF) of the Government of India, available at agriinfra.dac.gov.in, has listed NBFCs as eligible lending institutions — meaning agri businesses promoted by returning NRIs and international graduates can access AIF-backed loans through these NBFCs at interest-subvented rates. Explore agriculture jobs and finance opportunities at agrijob.in to find career paths alongside your agri-NBFC loan journey.

Important Links

| Resource | Link |

|---|---|

| RBI NBFC Official FAQ (April 2026) | rbi.org.in – NBFC FAQ PDF |

| NABARD Official Website | nabard.org |

| NABKISAN Finance Limited | nabkisan.org |

| NABSamruddhi Finance | nabsamruddhi.in |

| Kissandhan Agri Finance | kissandhan.com |

| Samunnati Financial Services | samunnati.com |

| NAFA (Netafim Agri Financing) | nafa.co.in |

| AIF Eligible Lending Institutions | agriinfra.dac.gov.in |

| More Agriculture Finance Guides | agrijob.in – Agri Finance |

| Latest Govt Jobs 2026 | agrijob.in – Govt Jobs 2026 |

| Join Telegram | agrijob.in Telegram |

Frequently Asked Questions about Agri-NBFCs in India 2026

Q1. What are Agri-NBFCs in India 2026?

Agri-NBFCs in India 2026 are RBI-registered Non-Banking Financial Companies that exclusively or primarily provide loans and financial services to the agriculture sector — including farmers, FPOs, agri-MSMEs, agri-traders, and rural entrepreneurs. They are faster, more flexible, and more specialised than traditional banks for farm sector credit.

Q2. Are Agri-NBFCs safe to borrow from?

Yes — provided the NBFC is listed in the RBI’s official NBFC register at rbi.org.in. Government-promoted NBFCs like NABKISAN (NABARD subsidiary) and NABSamruddhi (NABARD subsidiary) carry the highest credibility. Always verify RBI registration before applying and never pay any upfront fee before loan sanction.

Q3. What is the interest rate at Agri-NBFCs in India 2026?

Interest rates at Agri-NBFCs range from approximately 10% p.a. (NABKISAN / NABSamruddhi — government-backed) to 22% p.a. (smaller private microfinance-focused NBFCs). The rate depends on the NBFC, loan type, collateral, and the borrower’s credit profile. Commodity-backed and FPO loans tend to attract lower rates than unsecured rural loans.

Q4. What is the best Agri-NBFC in India for FPOs in 2026?

NABKISAN Finance Limited is widely regarded as the best Agri-NBFC for FPOs and PACS in 2026 due to its NABARD backing, concessional rates in partnership with state governments and NCDEX, and explicit focus on Farmer Producer Organisations. Samunnati is a strong second choice for FPOs seeking both finance and market linkages.

Q5. Can NRIs or Indian students abroad access Agri-NBFC loans?

NRIs cannot directly hold agricultural land under FEMA, but Agri-NBFC loans for agri-businesses (FPOs, food processing, agri-tech) are accessible through resident co-applicants or Indian-registered companies. Indian citizens studying abroad can apply directly upon return. AIF-backed NBFC loans are particularly suitable for returning agri-graduates setting up innovative farm ventures.

Q6. How fast do Agri-NBFCs disburse loans in 2026?

Top Agri-NBFCs disburse loans in 3–15 working days — significantly faster than traditional PSBs (15–60 days). Kissandhan’s phygital model and Samunnati’s digital processes allow some loans to be sanctioned within 72 hours for existing customers with clean credit history.

Final Thoughts on Agri-NBFCs in India 2026

Agri-NBFCs in India 2026 represent one of the most dynamic and impactful segments of India’s rural financial ecosystem. Whether you are a small farmer needing commodity-backed working capital, an FPO seeking institutional finance, an agri-MSME requiring invoice discounting, or a returning agri-graduate building an innovative farm business — there is an RBI-regulated Agri-NBFC in 2026 tailored to your exact need. Always verify RBI registration, compare interest rates, and match the loan product to your specific requirement before applying. Visit agrijob.in for more agriculture finance guides, government scheme updates, and the latest agriculture job notifications across India.

Disclaimer: This Agricultural jobs related information is only for the purpose of providing information to you and for Agricultural career advancement of Agricultural, Horticulture, Agronomy, Soil Science, Plant Breeding, Agriculture Marketing, Forestry, Poultry, Fisheries, Agri Business Management Graduates. We are not representing this employer or any Employment Agency nor we guarantee any employment. We do not ask candidates for any fees, Personal Information like (Bank OTP, Credit-Debit Card No, Aadhar Card OTP etc.) Please be Aware And never Share Such Information to any one or In the Name of agrijob.in. Please verify the correctness of the Agri jobs details yourself. We do not offer any guarantee on correctness of any details mentioned here. If a candidate pays any amount to anyone claiming to represent any company then it would be the responsibility of that candidate and he cannot hold us or the concerned employer responsible for such fraudulent activities.