Parametric Crop Insurance India 2026 – How Satellite-Based Weather Insurance Works

Parametric crop insurance India is rapidly transforming how millions of farmers protect their livelihoods against unpredictable weather. Unlike traditional crop insurance that requires field inspections and takes months to settle claims, satellite-based weather insurance in India uses real-time NDVI data, automated weather stations, and AI-driven yield estimation to trigger payouts automatically — often within 30 days of a weather event. In 2026, with the Union Cabinet having extended PMFBY and RWBCIS with a record allocation of Rs.69,515.71 crore and dedicating Rs.824.77 crore to technology platforms like YES-TECH and WINDS, parametric agriculture insurance has entered its most important phase in India’s history. This complete guide explains how satellite-based crop insurance works, the RWBCIS parametric model, NDVI triggers, payout mechanisms, the YES-TECH and WINDS framework, and how Indian farmers can benefit in 2026.

| Flagship Scheme | PMFBY + RWBCIS (Parametric arm) |

| Nodal Ministry | Ministry of Agriculture & Farmers Welfare, Govt. of India |

| Total Allocation (2021–26) | Rs.69,515.71 crore |

| Technology Fund (FIAT) | Rs.824.77 crore for YES-TECH & WINDS |

| Farmer Premium (Kharif) | Only 2% of Sum Insured |

| Farmer Premium (Rabi) | Only 1.5% of Sum Insured |

| Farmer Applications (2016–2024) | 56.80 crore enrolled |

| Claims Paid (Total) | Rs.1,55,977 crore to 23.22 crore applicants |

| Claim Return Per Rs.100 Premium | Rs.500 (5x return for farmers) |

| Satellite Technology Used | Sentinel-2, ResourceSat, NDVI, SAR, LSWI |

| Parametric Market Growth | ~11.3% CAGR projected through 2028 |

| Official Portal | pmfby.gov.in |

- What Is Parametric Crop Insurance India?

- PMFBY vs RWBCIS – Traditional vs Parametric Model

- How Satellite-Based Crop Insurance Works in India 2026

- YES-TECH – Yield Estimation System Using Technology Explained

- WINDS – Weather Information & Network Data System Explained

- NDVI & Satellite Indices Used as Parametric Triggers

- How Parametric Payouts Reach Farmers – Step by Step

- Premium Structure & Government Subsidy Breakdown 2026

- Basis Risk in Parametric Crop Insurance – The Core Challenge

- Parametric vs Traditional Crop Insurance – Full Comparison

- Who Benefits Most from Parametric Crop Insurance India?

- High-Value Agri Insurance & FinTech Terms You Must Know

- Frequently Asked Questions (FAQ)

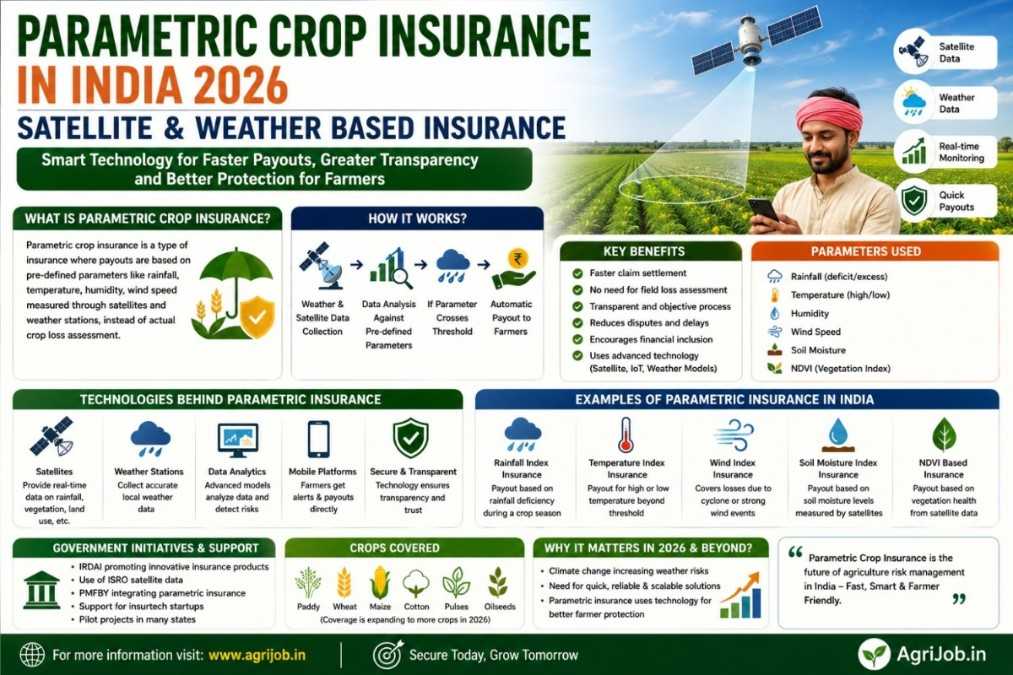

What Is Parametric Crop Insurance India? – The 2026 Definition

Parametric crop insurance India — also known as index-based crop insurance — is a financial protection mechanism where insurance payouts are triggered automatically when a pre-defined measurable parameter crosses a threshold, rather than requiring physical loss assessment of each farmer’s field. In 2026, this parameter is typically one of these: cumulative rainfall below a set level (measured by automated weather stations), temperature exceeding a crop-damaging threshold, or a vegetation health index (NDVI) dropping below a seasonal baseline captured via satellite imagery.

The word “parametric” comes from “parameter” — a measurable, independently verifiable variable. The insurance contract specifies the exact parameter, the trigger threshold, and the payout amount upfront. When satellite data or weather station data confirms the trigger is crossed, the payout is processed — no adjuster, no inspection, no delay. This is why parametric agriculture insurance is transforming India’s rural risk management landscape: it delivers speed, transparency, and objectivity that the traditional indemnity model cannot.

India’s parametric crop insurance market is projected to grow at approximately 11.3% CAGR through 2028, with agriculture accounting for nearly 50% of all early parametric product uptake nationally. As climate extremes intensify — with droughts, unseasonal rains, and heat waves hitting Bihar, UP, Maharashtra, Rajasthan, and other major farming states harder every year — the case for fast, objective, satellite-driven crop insurance has never been stronger.

PMFBY vs RWBCIS – Traditional Indemnity vs Parametric Weather Model

India operates two parallel national crop insurance architectures in 2026. Understanding the difference between PMFBY (Pradhan Mantri Fasal Bima Yojana) and RWBCIS (Restructured Weather Based Crop Insurance Scheme) is essential for farmers, agronomists, and policy researchers:

| Parameter | PMFBY (Area-Yield / Indemnity) | RWBCIS (Parametric / Weather Index) |

|---|---|---|

| Insurance Type | Area-yield indemnity insurance | Parametric weather index insurance |

| Payout Trigger | Yield shortfall vs historical average (via CCEs) | Weather parameter crossing pre-set threshold |

| Loss Assessment | Crop Cutting Experiments (field-based) | Automated weather stations + satellite data |

| Settlement Speed | 60–120 days (data-dependent) | 14–30 days (automated trigger) |

| Risks Covered | Drought, flood, cyclone, pest, disease, hailstorm | Rainfall deficit/excess, temperature extremes, humidity, wind |

| Farmer Premium (Kharif) | 2% of sum insured | 2% of sum insured (same) |

| Basis Risk | Low (individual-level assessment) | Moderate (being reduced via WINDS) |

| Technology Use | Satellite + drones for yield estimation (YES-TECH) | AWS + satellite NDVI as primary trigger |

| Best For | Multi-risk coverage including pest & disease | Weather-dominant risk regions (rain-fed areas, drought zones) |

Both schemes were extended by the Union Cabinet through FY 2025-26 with a combined outlay of Rs.69,515.71 crore — an increase from the previous Rs.66,550 crore allocation. The northeast states receive a special 90% central subsidy on premium, compared to 50:50 Centre-State sharing in other regions.

How Satellite-Based Crop Insurance Works in India 2026 – Step by Step

Satellite-based crop insurance 2026 in India follows a data-driven workflow that eliminates the need for individual field inspections. Here is exactly how the system operates from enrollment to payout:

- 🌾 Farmer Enrollment: Farmers register on the PMFBY/RWBCIS portal at pmfby.gov.in with their Aadhaar, land records (7/12 extract or Khasra-Khatauni), bank account details, and crop information. Loanee farmers with KCC loans may be auto-enrolled (voluntary since Kharif 2020).

- 🗺️ Geofencing & Field Mapping: The insured field’s GPS coordinates are captured via mobile app. Satellite imagery (Sentinel-2 at 10m resolution, ResourceSat-2 at 5.8m) is geo-referenced to each enrolled field or Insurance Unit (IU), typically a group of villages at gram panchayat level.

- 🛰️ Continuous Satellite Monitoring: Throughout the crop season (Kharif: June–October; Rabi: November–March), satellites pass over the insured area every 5–10 days capturing NDVI, LSWI (Land Surface Water Index), SAR backscatter, and FAPAR data. This tracks crop health, water stress, and vegetation density in near-real-time.

- 🌡️ Weather Station Data Integration: Under WINDS, automated weather stations (AWS) and rain gauges installed at block/panchayat level transmit real-time rainfall, temperature, wind speed, and humidity readings to the PMFBY central data platform.

- ⚡ Trigger Activation: If satellite-derived indices (NDVI below seasonal baseline) or weather station data (cumulative rainfall below trigger level, temperature above crop threshold) breach the pre-defined parametric trigger, the insurance system automatically flags the affected Insurance Units for payout processing.

- 🔢 Yield Estimation via YES-TECH: Under the YES-TECH framework, satellite data contributes at least 30% weightage to crop yield estimation for the affected IU. The remaining 70% can be from Crop Cutting Experiments (CCEs) — but the goal is to progressively increase satellite weightage to 70%+ as data quality improves.

- 💳 Direct Benefit Transfer (DBT): Once the yield shortfall or weather trigger is confirmed, claims are calculated and paid via DBT directly to farmers’ Aadhaar-linked bank accounts. Updated PMFBY guidelines mandate settlement within 30 days of yield data availability, with a 12% penalty on insurers for delays (effective Kharif 2024).

YES-TECH – Yield Estimation System Using Technology Explained

YES-TECH (Yield Estimation System using Technology) is a landmark shift in how India measures crop yields for insurance purposes. Funded by the Rs.824.77 crore FIAT (Fund for Innovation and Technology) corpus, YES-TECH replaces the slow, expensive, and dispute-prone manual Crop Cutting Experiment (CCE) system with satellite and remote sensing data.

- 🛰️ Satellite Data Sources: YES-TECH integrates multi-source satellite data — ISRO’s ResourceSat-2/2A, ESA’s Sentinel-1 (SAR) and Sentinel-2 (optical), and MODIS — to generate crop maps, growth stage identification, and yield estimation models at the Insurance Unit level.

- 📊 Minimum 30% Technology Weightage: As per current PMFBY operational guidelines, YES-TECH data must constitute a minimum of 30% of the final yield estimate used for claim computation. ICAR and SAC (Space Applications Centre, Ahmedabad) are working towards increasing this to 70% by 2027.

- 🤖 AI and Machine Learning Integration: YES-TECH uses machine learning regression models trained on historical yield data, satellite time series (NDVI, EVI, LSWI), and ground-truth CCE data to predict crop yields at 30m resolution. This allows estimates even for small, fragmented landholdings typical in Bihar, UP, and West Bengal.

- ⏱️ Faster Claim Trigger: Because YES-TECH can generate preliminary yield estimates within 2–4 weeks after harvest — versus 3–4 months for traditional CCE-based data — it dramatically accelerates the claim settlement timeline for farmers under satellite-based crop insurance 2026.

- 🔍 Dispute Reduction: By replacing subjective manual CCE measurements with independently verifiable satellite data, YES-TECH reduces the chronic disputes between farmers, state governments, and insurance companies that have historically delayed payouts under PMFBY.

WINDS – Weather Information & Network Data System Explained

WINDS (Weather Information and Network Data System) is India’s most ambitious weather infrastructure project for agriculture — also funded under the Rs.824.77 crore FIAT corpus. WINDS addresses the most critical gap in parametric crop insurance: the lack of hyper-local, reliable weather data at the field level.

- 📡 Automated Weather Station (AWS) Network: WINDS is building a dense network of automatic weather stations and rain gauges at the block and gram panchayat level across India’s major agricultural districts. Each AWS captures rainfall, temperature (max/min), relative humidity, wind speed/direction, and solar radiation every 15 minutes.

- 🌧️ Hyper-local Data Granularity: Traditional India Meteorological Department (IMD) stations cover large areas — often one per district. WINDS targets one AWS per Nyaya Panchayat (sub-block), bringing weather data granularity down to the 5–10 km radius level — critical for accurate RWBCIS parametric triggers.

- 🔗 Real-time Data Transmission: All WINDS stations transmit data in real-time to the National Crop Insurance Portal (NCIP) via IoT-enabled data loggers. Insurance companies and state governments access this data live through APIs integrated with the PMFBY platform.

- 📉 Basis Risk Reduction: The primary benefit of WINDS for parametric agriculture insurance model India is dramatic basis risk reduction. When AWS coverage is dense enough, the weather trigger reflects conditions much closer to the actual farm — reducing the mismatch between trigger activation and real farmer loss.

- 🏛️ Integration with RWBCIS: WINDS data directly feeds the weather-based crop insurance scheme RWBCIS trigger models. In pilot districts, WINDS-based RWBCIS has shown claims settlement within 14 days of a trigger event — compared to the 60–120 day average under traditional PMFBY.

NDVI & Satellite Indices Used as Parametric Triggers in 2026

In 2026, satellite-based crop insurance India uses a suite of vegetation and atmospheric indices as parametric triggers. Understanding these indices is important for agriculture professionals, insurance companies, and policy researchers:

| Index / Parameter | Full Name | What It Measures | When Used as Trigger |

|---|---|---|---|

| NDVI | Normalized Difference Vegetation Index | Crop canopy health, greenness, biomass density | Active crop growth stage (Kharif: Aug–Sep; Rabi: Jan–Feb) |

| LSWI | Land Surface Water Index | Crop water content, soil moisture, waterlogging | Flood detection and drought stress monitoring |

| SAR Backscatter | Synthetic Aperture Radar Backscatter (Sentinel-1) | Crop structure, lodging detection, waterlogging under clouds | Monsoon season (cloud-penetrating capability) |

| FAPAR | Fraction of Absorbed Photosynthetically Active Radiation | Crop photosynthetic efficiency and productivity | Mid-season stress assessment |

| MSAVI | Modified Soil-Adjusted Vegetation Index | Early-stage crop emergence (minimises bare soil interference) | Crop establishment period (June–July for Kharif) |

| Rainfall Index (RWBCIS) | Cumulative Rainfall from AWS / IMD Grid | Total precipitation during critical crop phases | Deficit rainfall trigger (drought) or excess trigger (flood) |

| Temperature Index | Max/Min Temperature from AWS | Heat stress on crop, frost damage | Rabi: frost trigger (wheat, mustard); Kharif: heat stress trigger |

In 2026, the most advanced parametric frameworks use a composite index (Crop Health Factor — CHF), which combines NDVI, LSWI, SAR backscatter, FAPAR, rainfall, and rainy-day count into a single score ranging from 0 to 1. This approach was piloted in West Bengal on 3.5 million hectares of paddy in 2020, covering 3,200 Insurance Units — and has since informed the national YES-TECH design.

How Parametric Payouts Reach Farmers – Step by Step 2026

The payout mechanism for parametric crop insurance India 2026 is designed for speed and transparency. Here is how a farmer actually receives their claim after a weather trigger:

- 📡 Trigger Detection: AWS (WINDS network) or satellite system records that the parametric threshold has been breached — e.g., rainfall in the block has been less than 50mm during the critical 4-week Kharif sowing phase.

- 🖥️ Automatic System Alert: The National Crop Insurance Portal (NCIP) at pmfby.gov.in automatically flags all enrolled farmers in the affected Insurance Unit (gram panchayat / block). Insurance company dashboards show the triggered zone in real-time.

- ✅ Verification & Claim Computation: For RWBCIS parametric claims, no individual field verification is needed — the weather data is the evidence. The insurance company computes payouts using the pre-agreed indemnity schedule (e.g., deficit rainfall of 10mm below trigger = Rs.500/acre payout).

- 🏦 State Government Approval: The computed claim list is shared with the State Agriculture Department for approval. Under updated PMFBY guidelines, state governments must clear claims within 3 weeks of receiving the list — delays attract penalties.

- 💸 DBT Transfer: Approved claim amounts are transferred via Direct Benefit Transfer (DBT) to each farmer’s Aadhaar-seeded bank account through the PFMS (Public Financial Management System). Farmers receive an SMS notification on claim credit.

- 📱 Tracking via App: Farmers can track claim status in real time on the PMFBY mobile app or by visiting pmfby.gov.in → Farmer Corner → Claim Status. The app shows trigger date, claim amount, and DBT transfer date.

Premium Structure & Government Subsidy – Parametric Crop Insurance 2026

| Crop Season | Farmer Premium | Actual Actuarial Premium | Govt. Subsidy (Central + State) | Example: Farmer Pays on Rs.1L SI |

|---|---|---|---|---|

| Kharif (June–Oct) | 2% of Sum Insured | 10–15% | 8–13% (shared 50:50, Centre:State) | Rs.2,000 only |

| Rabi (Nov–Mar) | 1.5% of Sum Insured | 10–15% | 8.5–13.5% | Rs.1,500 only |

| Commercial / Horticulture | 5% of Sum Insured | 10–20% | 5–15% | Rs.5,000 only |

| Northeast States (All Seasons) | Same as above | Same as above | Centre: 90%, State: 10% | Same farmer share |

For every Rs.100 of premium paid by farmers across 8 years of PMFBY, farmers have received approximately Rs.500 in claims — a 5x return ratio that makes India’s crop insurance scheme one of the most farmer-favourable in the world. The total government subsidy burden of Rs.69,515.71 crore for 2021–26 reflects India’s commitment to making parametric crop insurance economically accessible for small and marginal farmers.

Basis Risk in Parametric Crop Insurance India – The Core Challenge & 2026 Solutions

Basis risk is the defining challenge of parametric crop insurance. It occurs when a farmer suffers real crop loss — but the parametric trigger is not activated because the weather station or satellite data for their Insurance Unit does not cross the threshold. Or conversely, the trigger fires (payout made) but the farmer’s crop is actually fine.

- ⚠️ Spatial Basis Risk: When one farm 2km from the nearest AWS gets flooded but the station records acceptable rainfall, the farmer gets no payout. WINDS’ hyper-local AWS network — targeting one station per Nyaya Panchayat — is the primary 2026 solution to spatial basis risk in India.

- ⚠️ Temporal Basis Risk: A brief but intense hailstorm damages crops in one specific week but the monthly rainfall average stays normal. Parametric products now use weekly or phase-wise triggers (critical crop growth phase rainfall) instead of seasonal totals to address this.

- ⚠️ Crop-specific Basis Risk: NDVI thresholds must be calibrated per crop type, agro-climatic zone, and growth stage. A rice field and a wheat field in the same district will have vastly different NDVI baselines. YES-TECH’s multi-crop, multi-zone calibration models address this directly.

- ✅ Hybrid Product Solution: The most progressive 2026 approach combines parametric and indemnity coverage — parametric layers handle fast-payout weather risks (drought, flood, heat), while traditional indemnity layers cover complex losses (pest infestations, localised calamities). This hybrid model significantly reduces residual basis risk.

Parametric vs Traditional Crop Insurance – Complete 2026 Comparison

| Factor | Parametric / Weather Index (RWBCIS) | Traditional Indemnity (PMFBY) |

|---|---|---|

| Claim Trigger | Index crosses threshold automatically | Actual measured crop yield shortfall |

| Field Inspection | Not required | Crop Cutting Experiments (CCEs) mandatory |

| Settlement Speed | 14–30 days | 60–120 days (data collection delay) |

| Fraud Risk | Very low (satellite + AWS data) | Higher (CCE manipulation reported) |

| Transparency | High (pre-defined, publicly known triggers) | Moderate (CCE results opaque) |

| Basis Risk | Present; reduced by WINDS + satellite | Low (actual loss measured) |

| Administrative Cost | Lower (no field teams needed) | Higher (CCE teams, field adjusters) |

| Risk Coverage | Weather risks only (rain, temp, wind, humidity) | Multi-risk (weather, pest, disease, localised) |

| Best For Farmer | Rain-fed, drought-prone, weather-vulnerable areas | Irrigated farms, diverse risk exposure areas |

For India’s 140 million small and marginal farming households — 80% of whom operate rain-fed farms in climate-vulnerable districts — parametric crop insurance via RWBCIS with WINDS and YES-TECH is the superior model for weather risks. It delivers speed, objectivity, and lower administrative costs. However, for comprehensive protection including pest, disease, and localised calamity risks, PMFBY’s indemnity framework remains essential. The ideal 2026 architecture is a hybrid: parametric for weather, indemnity for complex risks — and India is moving in this direction.

Who Benefits Most from Parametric Crop Insurance India 2026?

- 🌾 Rain-fed Small Farmers (Bihar, UP, MP, Odisha, Jharkhand): Farmers in chronically drought-prone or flood-vulnerable districts who need fast post-event liquidity gain most — a parametric payout in 14–30 days allows immediate replanting or debt servicing, preventing distress migration.

- 👩🌾 Women Farmers and SHG Members: Schemes like JEEViKA in Bihar are enrolling SHG members in PMFBY/RWBCIS. Automatic DBT to their Aadhaar-linked accounts bypasses male household members and delivers financial empowerment directly.

- 📱 Tech-Savvy Young Farmers: Millennials running family farms who can track claim status on mobile apps, report crop loss with geotagged photos, and understand index-based triggers — they are the prime adopters of parametric crop insurance 2026 digital infrastructure.

- 🏦 Agri-Lending Banks (KCC Portfolios): Kisan Credit Card (KCC) lenders benefit massively from PMFBY/RWBCIS — insured farmers have demonstrably lower loan default rates post-crop failure. Parametric speed means farmers repay loans faster.

- 🌡️ Horticulture and High-Value Crop Farmers: Vegetable, flower, and fruit farmers face acute weather risks and high investment per acre. Temperature and humidity-triggered parametric products designed for these crops (5% premium) are growing rapidly in 2026.

- 🔬 AgriTech Startups and InsurTech Companies: Private insurers and AgriTech platforms building drone surveillance, satellite analytics, and AI underwriting tools are benefiting from FIAT-funded YES-TECH data standards that create a common platform for private parametric product innovation.

- 🏛️ State Governments with Climate-Exposed Districts: States like Bihar (floods), Rajasthan (drought), Vidarbha in Maharashtra (dryness), and coastal Odisha (cyclones) can use RWBCIS parametric models to build state-specific weather triggers calibrated to their agro-climatic zone — funded partly by FIAT.

- 📊 Agri-Researchers and UPSC / BPSC Aspirants: Parametric crop insurance, PMFBY, RWBCIS, YES-TECH, and WINDS are high-frequency topics in UPSC CSE, BPSC, and state agriculture department exams — understanding the framework deeply aids competitive exam preparation.

High-Value Agri Insurance & AgriTech Terms You Must Know in 2026

- 📌 Parametric Crop Insurance India: Index-based agricultural insurance where payouts are triggered by satellite or weather data crossing pre-set thresholds — eliminating field inspections and enabling 14–30 day settlements. India’s RWBCIS is its primary national implementation.

- 📌 RWBCIS (Restructured Weather Based Crop Insurance Scheme): India’s government-backed parametric weather insurance model covering losses from adverse rainfall, temperature, wind, and humidity. Premium is subsidised at 2% (Kharif) and 1.5% (Rabi) for farmers.

- 📌 YES-TECH (Yield Estimation System using Technology): Satellite and remote sensing-based crop yield estimation system funded by India’s Rs.824.77 crore FIAT corpus. Gives minimum 30% weightage to technology data in PMFBY claim computation — replacing slower manual CCEs.

- 📌 WINDS (Weather Information and Network Data System): India’s hyper-local weather station network at block/panchayat level — feeding real-time rainfall, temperature, and humidity data into RWBCIS parametric triggers. Core to reducing basis risk in satellite-based crop insurance.

- 📌 FIAT (Fund for Innovation and Technology): Rs.824.77 crore government corpus approved by the Union Cabinet to fund YES-TECH, WINDS, R&D, and digital infrastructure for modernising PMFBY and RWBCIS claim processes in India.

- 📌 Basis Risk: The gap in parametric insurance between actual farm-level loss and the triggered payout — the central design challenge of index-based crop insurance. Reduced by dense AWS networks (WINDS) and high-resolution satellite indices (NDVI at 10m resolution).

- 📌 NDVI (Normalized Difference Vegetation Index): The most widely used satellite index in crop insurance — measuring crop greenness and health. Derived from Sentinel-2 and ResourceSat imagery at 10–30m resolution. When NDVI drops below seasonal baseline, it triggers yield shortfall claims under YES-TECH.

- 📌 CHF (Crop Health Factor): A composite satellite-derived insurance index combining NDVI, LSWI, SAR backscatter, FAPAR, rainfall, and rainy day count into a single 0–1 score. Piloted in West Bengal paddy insurance (3.5M ha) — the model for India’s future national parametric crop insurance design.

- 📌 DBT (Direct Benefit Transfer): The payment mechanism through which crop insurance claims under PMFBY and RWBCIS are credited directly to farmers’ Aadhaar-linked bank accounts — eliminating intermediaries and reducing leakage in parametric payout disbursement.

- 📌 InsurTech Agriculture India: The emerging sector of technology-driven insurance companies (Kshema General Insurance, Niramai, Cropin, SatSure, Kheti Buddy) building AI underwriting, satellite NDVI monitoring, and mobile-first claim platforms on top of India’s PMFBY/RWBCIS framework — a high-growth career and investment space in 2026.

Frequently Asked Questions – Parametric Crop Insurance India 2026

What is parametric crop insurance in India?

Parametric crop insurance India is an index-based insurance where payouts are automatically triggered when a pre-defined weather or satellite parameter — rainfall below a threshold, NDVI dropping below baseline, or temperature above a crop-damage level — is breached. No field inspection is required. India implements this primarily through RWBCIS (weather triggers) and YES-TECH within PMFBY (satellite yield estimation). The market is growing at 11.3% CAGR and covers approximately 50% of all parametric product uptake in India as of 2026.

How does satellite-based crop insurance work in India 2026?

Satellite-based crop insurance 2026 in India uses Sentinel-2 (10m resolution), ResourceSat-2, and SAR imagery to monitor enrolled farm fields continuously through the crop season. NDVI, LSWI, FAPAR, and SAR backscatter indices are computed for each Insurance Unit. Under YES-TECH, these satellite indices carry a minimum 30% weightage in crop yield estimation. When the computed yield or weather parameter crosses the insurance trigger, payouts are processed via DBT within 30 days — with a 12% penalty on insurance companies for delays.

What is RWBCIS and how is it different from PMFBY?

RWBCIS (Restructured Weather Based Crop Insurance Scheme) is India’s parametric weather insurance model — payouts triggered by weather data (rainfall, temperature, humidity) crossing agreed thresholds. PMFBY is an area-yield indemnity scheme — payouts triggered by actual yield shortfall measured via Crop Cutting Experiments. RWBCIS settles claims in 14–30 days; PMFBY takes 60–120 days. Both are extended to FY 2025-26 with a combined Rs.69,515.71 crore outlay.

What is YES-TECH in crop insurance India?

YES-TECH (Yield Estimation System using Technology) is India’s satellite and remote sensing-based crop yield estimation framework funded by the Rs.824.77 crore FIAT corpus. It integrates satellite NDVI data with ground-level CCE data — giving satellite data a minimum 30% weightage — to compute crop yields faster and more objectively for PMFBY claims. YES-TECH reduces CCE dependence, speeds up settlement, and minimises farmer-insurer disputes over yield data.

What is WINDS in agriculture insurance?

WINDS (Weather Information and Network Data System) is India’s hyper-local automated weather station network being built under the FIAT corpus. It places AWS and rain gauges at the block/panchayat level to collect real-time rainfall, temperature, humidity, and wind data. WINDS feeds directly into RWBCIS parametric triggers and dramatically reduces basis risk by providing granular, on-the-ground weather data instead of interpolated district-level data from distant IMD stations.

What is basis risk in parametric crop insurance?

Basis risk is the mismatch between actual farmer crop loss and the parametric insurance payout. It occurs when a farm suffers loss but the weather station or satellite index for the Insurance Unit doesn’t breach the trigger threshold (under-payment), or when the trigger fires but crops are actually fine (over-payment). WINDS’ hyper-local AWS, satellite indices at 10m resolution, and composite CHF models are India’s 2026 strategies to minimize this core parametric insurance challenge.

What is the premium for crop insurance in India 2026?

Indian farmers pay only 2% of the sum insured for Kharif crops, 1.5% for Rabi crops, and 5% for commercial/horticultural crops under both PMFBY and RWBCIS. The actual actuarial premium (10–18%) is subsidised by the Central and State governments in equal shares (90:10 for Northeast states). On a Rs.1 lakh sum insured, a Kharif farmer pays just Rs.2,000 while receiving up to Rs.1 lakh in claims — an extraordinarily farmer-favourable structure.

How many farmers benefited from crop insurance in India 2026?

Since PMFBY launched in 2016 through 2024, 56.80 crore farmer applications have been enrolled and over 23.22 crore farmer applicants have received claims totalling Rs.1,55,977 crore. For every Rs.100 in premium paid by farmers, they received approximately Rs.500 in claims — making PMFBY the third-largest crop insurance scheme globally by premium volume. In a recent season alone, insurer Kshema facilitated the enrolment of over 5 lakh farmers with claims worth Rs.500 crore settled.

📌 Important Official Links:

- 🔗 PMFBY Official Portal – pmfby.gov.in (Enroll & Track Claims)

- 🔗 PM India – Cabinet Approval on PMFBY & RWBCIS Extension

- 🔗 Ministry of Agriculture & Farmers Welfare – agricoop.nic.in

- 🔗 ICAR – Indian Council of Agricultural Research (YES-TECH Research Partner)

- 🔗 Agriculture Government Jobs 2026 – Agrijob.in

- 🔗 Also Read: Bihar Agriculture Coordinator Vacancy 2026 – Agrijob.in

📅 Last Updated: May 2026 | This guide is regularly reviewed and updated with the latest data on parametric crop insurance India, RWBCIS, YES-TECH, WINDS, and PMFBY statistics. Bookmark this page for the most current satellite-based crop insurance updates. Stay connected with Agrijob.in — India’s #1 Agriculture Information Portal.

]]>